What Is Due Diligence in Business?

In business, due diligence is the process of making sure every aspect of a transaction is in order before it moves forward. When a company considers issuing an IPO, potential investors perform due diligence on that company to make sure it’s worth the investment. The term is sometimes used in the hiring process to verify that a candidate has the experience they claim.

Due diligence in M&A can include not only looking at obvious details like financial stability, sales, real estate, and intellectual property, but also pending litigation, labor relations, environmental problems, and relationships with third parties.

A Brief History of Due Diligence

The term due diligence, as related to transactions, entered common usage as a result of the U.S. Securities Act of 1933, specifically section 11b3, which says that sellers of securities have to give investors enough information to make an informed decision before buying. In this situation, the term meant "required carefulness" or "reasonable care." Since then, the expression has spread to other areas and has found its most common use in mergers and acquisitions.

The Role of Due Diligence

With proper due diligence, all involved parties are educated, informed, and covered in a transaction, an arrangement, or any other kind of agreement. Think of it like homework: It should be completed before the close of a deal to provide a buyer with a guarantee of what it’s getting.

In M&A, due diligence helps buyers and sellers make informed decisions. The process validates the accuracy of the information presented, ensures that the transaction complies with the criteria laid out in the purchase agreement, verifies that the parties consider all benefits and risks, and allows the buyer to know what they are buying.

Due diligence increases the chances of a successful deal by uncovering major problems or assets that need to be addressed. Additionally, due diligence can lead to a more accurate pricing of the transaction. Without proper due diligence, unforeseen problems may arise after the deal closes. At that point, they fall on the buyer, which may not be able to address them through litigation.

Charles Elson is the Director of the Weinberg Center for Corporate Governance at the University of Delaware, and co-author (with Alexandra Lajoux) of the book The Art of M&A Due Diligence: Navigating Critical Steps and Uncovering Crucial Data. He says, “[When] you're buying a business, you buy all kinds of potential liabilities, and you want to be clear on what are the pitfalls of the transaction.”

Certainly, due diligence incurs upfront costs, but the outlay is justified because it provides buyers and sellers with peace of mind and a level of comfort with their expectations. Ultimately, it helps ensure the buyer and the seller are equally knowledgeable about the transaction.

As Elson says, “You want to assure yourself that you've appropriately investigated the affairs of the counterparty so that [the] transaction, a year later, will be effective. It's a legal term basically offered from a director standpoint, meaning that you carry out your fiduciary responsibilities appropriately in terms of the transaction itself. It's there to protect you, from a legal standpoint, if things go bad.

“Basically,” he continues, “you're trying to understand the other person's business — ‘Is what I'm buying really going to be complementary to me? And will it not only be complementary, but also increase my value, or do I have a lot of problems in acquiring? If so, do I need to adjust the purchase price, or do I frankly need to even engage in the transaction?’ That's the issue. And there's just a ton of litigation around this stuff.”

Is There a Difference Between Due Care and Due Diligence?

In most areas of business, due care is not a well-defined concept. Informally, it means taking the steps that an ordinary, reasonable person would in similar circumstances, but is rarely used in business circumstances.

In IT — specifically, IT security — the two terms are different but related. With due care, the organization develops a structure that contains security protocols and procedures; with due diligence, it follows those protocols and procedures.

Some in the legal world say due care and due diligence are the same, but others contend they are different, albeit related in a manner similar to the IT description above.

Types of Due Diligence

Due diligence applies to many aspects of business. See how they’re used in the key areas listed below:

Mergers & Acquisitions

In an acquisition, a company buys another company (or even part of another company); a recent example is Amazon's purchase of Whole Foods. When two companies come together on equal terms, it’s a merger. In either case, due diligence helps companies do the following:

-

Make sure that all information reported by the seller is accurate.

-

Find and mitigate any risks.

-

Ensure compliance with legal and regulatory requirements.

-

Allow the deal to be priced based on facts, not assumptions.

Performing due diligence helps the buyer determine whether it actually will make the purchase and how much it should pay. The process may be voluntary in some cases and involuntary in others.

The concepts of soft and hard due diligence also come up within the M&A world. Hard due diligence is the traditional process described in this article. Soft due diligence focuses on culture fit and other elements related to how people work together. If the two cultures of the acquiring and target companies seem like they won’t combine well, then the companies may have to change personnel decisions, particularly with top executives and influential employees.

Securities Sales

The phrase due diligence was first used for securities sales. Specifically, securities sellers must disclose any material information they discover related to the securities that they plan to offer investors. If they fail to disclose such information, they are liable for criminal prosecution. Securities sellers research the offerings they are considering selling, the backers of the securities, the owners of the company, the performance history of the security, and other data in order to perform their analysis and uncover pertinent material information.

IPOs

Before a company's IPO, attorneys, underwriters, and the company itself have to prove to the SEC that the declarations the company made when filing are true. Key employees and those in the C-suite answer questions about areas such as the business plan (including marketing), product development, intellectual property, and revenue projections, with an eye to finding possible pitfalls. Third parties (e.g., vendors and customers) may be interviewed, as well. Companies can also expect an audit of their records, from HR to finance to licenses to tax filings and more.

Banking

Banking and financial services companies may perform due diligence on potential customers to make sure they are not involved in illegal activities that could bring legal action against the institution.

Enhanced Due Diligence

Due diligence is not always enough. In such cases, organizations perform enhanced due diligence, which is required when a potential banking customer poses a higher risk of being connected to money laundering, terrorist financing, or other financial crimes. A customer may run a higher risk due to their business activity, ownership structure, or anticipated or actual amount and types of transactions (this includes transactions that involve higher-risk jurisdictions).

In cases where enhanced due diligence is necessary, the bank should request the following information, both upon the creation of the account and on a recurring basis afterward:

-

Nature of the business

-

Purpose of the account and expected types of business transactions

-

Source of account funds and other assets

-

List of all individuals who have ownership or control over the account (e.g., beneficial owners, signatories, guarantors)

-

Type of businesses of all individuals with ownership or control over the account

-

Financial statements

-

Key business documents

-

References

-

Where the customer resides and the primary trade area

-

Where the business is located and the primary trade area

-

Proximity of the bank to the customer’s residence, place of business, and place of employment

-

Expectations of routine international transactions

-

Description of business operations, anticipated volume of transaction, and total sales

-

Major customers and suppliers

-

Explanations for any changes in account activity

The bank should also review the internet and news sources for negative mentions of the customer.

Simplified Due Diligence

Unlike enhanced due diligence, simplified due diligence means performing a less rigorous version of standard due diligence. The organization can implement simplified due diligence when the customer runs a very low risk for money laundering, terrorist financing, or other financial crimes. This term is more prevalent in the European Union and a few Asian countries than in the United States.

Contingent Due Diligence

Contingent due diligence is a term used in real estate to designate one of the status periods before the deal is final. During the contingent due diligence phase, the buyer can terminate the deal without penalty (generally for any reason).

Due Diligence in Others Areas of Business

The term due diligence is also used by financial advisors and in private equity funding.

Why Due Diligence Is Important

The process of due diligence serves numerous functions that benefit both buyers and sellers in a merger or acquisition. These benefits include the following:

-

Allows a buyer to confirm financial, contract, customer, and other pertinent information about the seller

-

Paints a fuller picture of the scope of the transaction, including discovery of previously unknown problems and assets

-

Leads to more accurate pricing (the initial offer could rise or fall, depending on what due diligence uncovers) because decisions are better informed

-

Permits the buyer to back out of a deal if due diligence uncovers problems that are too big or complex to address

-

Creates greater awareness, clearer expectations, and increased comfort for the buyer and seller of what’s expected of them to close the deal

-

Reduces the knowledge gap between buyer and seller, leading to better (and better-informed) decisions

The Challenges of Due Diligence

Due diligence poses a number of challenges. Working through these issues is essential to ensuring that the process reveals all connected information and the transaction is performed legally.

-

It can be difficult to ensure that the parties meet all applicable legal and regulatory requirements. In the United States, this includes the Sarbanes-Oxley Act.

-

Buying a private company draws more scrutiny than buying a publicly traded company, as private companies haven't gone through the examination required for a public offering.

-

If the deal includes international components, companies must comply with the Foreign Corrupt Practices Act and international accounting standards.

-

Every deal is unique, so every process has to be customized. This is even more complicated with the different types of M&A structures — for example, a stock transaction versus cash or an acqui-hire (i.e., buying a company to gain key personnel).

-

Sellers may not be ready to step aside after you complete the deal. This is hard to plan for, and due diligence can’t uncover it.

-

It may take 12 to 16 months for a certified exit planning advisor to prepare a transition plan.

-

Sellers may not start preparing information soon enough. It should happen when the company is being shopped around, not after the deal is signed. Deals often fail due to inadequate preparation and transition planning.

-

Companies must keep on top of changing regulations, such as a recent decision on mergers made by the Delaware Chancery Court (and upheld by the Delaware Supreme Court).

-

Sellers may be reticent to provide all information requested by the buyer, especially if it’s negative and may impact the final price, or if it takes lot of time to gather.

Brett Cenkus is an attorney with over 20 years of experience in mergers and acquisitions, and the owner for Cenkus Law. “Sellers view [due diligence] as a necessary evil to get the deal done, but underneath it are a bunch of benefits,” he says. “A buyer who isn't getting the information they need is going to be concerned about closing; things slow down when they're not getting what they're looking for. If there's any effort to sort of sidestep an issue, it has legal ramifications.

“The truth is, you’re better off with a buyer by making them comfortable and giving that information. You don't want a buyer who doesn't know what they bought. A lot of sellers don't appreciate that these buyers want to buy your company — they're spending money and time, so this is an opportunity to be sure they own all of it.”

How Can Companies Use Due Diligence?

The questions raised during due diligence should drive further investigation.

“If you find something that appears problematic, you have to do further investigation,” says Elson. “In other words, if something comes to your attention that appears problematic, you then need to determine how serious is the issue. Does it affect the price of the transaction? Or more concerning, does it affect the ability to enter in the transaction at all?”

Due diligence also protects shareholders by determining if the transaction makes sense in terms of valuation.

Once the companies complete their due diligence, the process will drive one of the following results for the proposed deal:

-

Repricing

-

Changing the terms or scope

-

Canceling

-

Moving forward as originally planned

A letter of intent (LOI) is a document that states the buyer and seller are negotiating a merger or acquisition but have not yet reached a final agreement. Most LOIs have a material adverse change (MAC) clause that allows the parties to change or terminate the deal if new information comes out.

When to Conduct Due Diligence

Due diligence takes time. Sellers should prepare as much as they can before they sign a deal — in other words, the target company should compile the basic information while the company is being marketed (two or three months is a realistic timeline). The seller may have a formal auction to draw bids from multiple buyers.

After the parties sign a letter of intent, the process truly begins. The parties should complete due diligence before the deal is scheduled to close, so there's time to fix problems, change the price, or cancel the transaction.

How Long Does Due Diligence Take?

While the LOI will delineate a time frame for due diligence, the general consensus is 30-60 days, but each merger or acquisition is different. Due diligence might run longer or shorter; the benchmark time frame exists to ensure that the due diligence process doesn’t become a sprawling, unending monster with no end in sight.

Consider the following when setting a timeline:

-

The complexity of the deal (e.g., how many subsidiaries does the acquired company have?)

-

What business (industry and vertical) is the acquired company in?

-

How large is the target company?

-

What kind of merger or acquisition is it?

-

Are any international properties involved in the deal?

-

The legal portion of the process can take 10-20 percent of your time and effort, and other portions take up the remaining 80-90 percent.

Can Companies Extend Due Diligence?

You can prolong due diligence, but the process may grow without boundaries. You should avoid extensions unless absolutely necessary.

Can Companies Capitalize Due Diligence Costs?

The answer is complicated. The buyer should always consult legal and financial professionals to ensure that they are categorizing the costs correctly.

For accounting purposes, due diligence and other acquisition-related costs cannot be capitalized and must be considered as expenses.

Charles Elson of the University of Delaware says, “You thought that [an M&A deal] was going to be treated one way, tax-wise, and instead the transactions treated another. It kills the economics of it. Taxation is very significant in this process.”

For tax purposes, due diligence and other acquisition-related costs may be treated as capital expenses if they occur on or after the bright line date. On this date, the seller indicates they are committed to moving forward with the merger or acquisition, demonstrated by either the execution of an LOI or by the buyer’s board of directors authorizing or approving the terms of the transaction.

If one or both companies abandons the deal, the parties will probably not be able to capitalize the costs of due diligence for tax purposes.

Who Can Conduct Due Diligence?

Due diligence is a demanding, high-pressure process that requires a lot of skill and expertise. The buyer is the primary responsible party, but they can bring in third-party advisors for support (companies with a lot of experience may perform the entire process in-house). External consultants could range from a single person for a small deal to a vast team for a multinational corporation. Regardless of the size of the buyer and the advisory team, the buyer should try to engage both internal and external experts to help them evaluate the deal (based on available funds). These experts should include the following:

-

M&A attorneys (for smaller deals, using an outside expert to lead the process allows the buyer and seller to focus on running their existing businesses)

-

Attorneys and experts in common fields, such as labor

-

Attorneys and experts in fields specific to the transaction (e.g., environmental authorities for the purchase of a oil spill cleanup company)

-

Accountants, including CPAs

-

Bankers

-

PMOs

-

Analysts

-

MBAs

-

Limited partners

-

VCs (for larger deals, if outside funding is needed to complete the deal)

-

Specialized consultants

Seller Due Diligence

Sellers can also conduct due diligence on potential buyers before offers come in (this often happens when buyer stock is part of the purchase). They can thus weed out weak bids, preventing wasted time and effort.

Who Can Prepare a Due Diligence Report?

The people and teams (both internal and external) involved in the due diligence process should prepare the report based on their findings. Larger buyers may bring in the corporate development team, or they may outsource the task to a third party.

Crucial Targets in the Due Diligence Process

The due diligence lifecycle is different for each kind of business. Key steps are outlined below for each business type.

Mergers & Acquisitions

Before they can put up a company for sale, the sellers need to do their work — some of which is later used in the due diligence process. Key preliminary due diligence actions include the following:

-

Strategy planning and preparation

-

Exit planning (the seller determines how to transition out of the business once it’s sold)

-

Formal marketing of the sale of the business

Both buyers and sellers must sign nondisclosure agreements (NDAs) and confidentiality agreements along with — or, for some key people, before — the LOI. Then due diligence begins. The seller sends a confidential information memorandum (CIM), also called a deal book, which provides crucial information about the company.

One of the first steps is to establish a document exchange. Pre-internet, this required a team to visit (often multiple times) the seller’s location and physically handle documents. Much of this work can now be done via a secure online data repository. The parties can post documents and grant access to those who need to see them. They also have the luxury of accessing documents at any time from their own office. However, site visits are still important.

“The ability to go to an operation and actually meet and greet people is a good thing,” says Elson. “Going to an operation and sitting there, feeling it, seeing it, understanding how people come together is an important part of the process … you don’t conduct due diligence merely on the internet.”

During due diligence, you may repeat a number of steps if new information comes to light:

-

Analysis of the purpose of the project (i.e., if the deal still meets business goals)

-

Analysis of the financial business case

-

Review of key documents

-

Risk analysis

-

Analysis of offer price (which may be tweaked based on discovery)

The results of the due diligence process (which should be compiled in a final report) will indicate whether or not you should move forward with the deal. If you do, negotiation then takes place, and you can make a final offer.

After the close of the deal, the companies issue a final announcement regarding the transaction. From there, they begin integrating functions, staff, and operations.

Securities Sales

Due diligence is used mostly for securities, but it can also apply to debt. When investigating securities, financial advisors should look at the following areas (at a minimum):

-

Market capitalization (total value) of the company

-

Revenue, profit, and margin (investments, net income)

-

Competitors and industries

-

Valuation multiples (e.g., price-to-earnings ratio)

-

Management and share ownership

-

Balance sheet (bond ratings, dividends paid, debt-to-equity ratio)

-

Stock price history

-

Stock options and dilution possibilities (e.g., 10-Q and 10-K reports)

-

Expectations

-

Long- and short-term risks

-

The amount of stock that the executives own

-

Income and revenue estimates for the next two to three years

-

Any long-term trends that might affect the corporation

-

Details about partnerships, joint ventures, IP, and new merchandise/companies

While advisors may not be legally obligated to perform due diligence on funds they recommend, it's a smart move to preserve the portfolios of your clients.

IPOs

A company trying to launch an IPO, in tandem with attorneys and underwriters, must focus on the registration statement. They will have to substantiate all claims made in the document in order to comply with state and federal security laws. Large investors should conduct their own due diligence, ensuring the company’s product or service is promising, considering an investment partnership to share the risks, developing a strategy to harvest returns over time, and planning an exit strategy in case the company fails.

Due Diligence Techniques

Regardless of the business area, communication is key both during and after due diligence. The concept of 360-degree communications, wherein you keep all required parties up to date, is a good rule of thumb. This doesn't mean everybody gets to know everything, however. Create a communication plan before due diligence, so you have a prepared strategy once you get underway.

“The people who are doing the implementation … don't know the company well, like the C-suite, who don't really want to do that work,” says Brett Cenkus. “It starts by having a good connection between who's going to execute and who’s [going to] set it all up.”

Both the buyer and seller should set up a structure for the process. As Cenkus explains, “From the seller’s standpoint, put the information out there in a very clear, structured manner. It's really as simple as organizing the information, and being out ahead of it in a really structured manner.

“On the buyer’s side, it's similar,” he continues. “If they're not organized in the information they're asking for, and not having high enough level people in the weeds, at least at the beginning, to be sure they can push the whole process out the door in a structured manner.

“The process, at least at the beginning, if it's going to be set up right, requires high-level input from the people who know where the bodies are buried (if it’s the seller) or what they're looking (if it’s the buyer),” Cenkus concludes.

This structure should include some centralization to avoid duplication of work and propagation of errors. The buyer and seller should each appoint a gatekeeper.

“From the seller's standpoint, to flow through one person and know exactly what's been requested can feel like a little bit of an impediment if the buyer starts dealing directly with the seller’s people,” explains Cenkus. “But that really starts to create problems.

“Number one, you don't have a good record of what's being communicated. Number two, what was communicated could be incorrect or not structured right. Number three, there's repeat questions. People start to get really frustrated in that administrative flow.

“From the buyer’s standpoint,” he continues, “the problem is even worse, which is where you want to make sure that everyone who needs information is getting it. So it's really [about] centralization. It feels like a little bit of an impediment to how the process is run overall, but it will make it smoother and make sure there aren't holes in the process.”

It’s a good idea to use a due diligence checklist to keep track of in-progress and completed items. That way, you can document and manage every detail as you move through the process.

Cenkus adds, “When you're able to give it [information] in a structured way and be very forthright, it makes buyers feel more comfortable and helps get deals closed.”

During due diligence, SWOT analysis can help you manage the process and stay focused on areas that need the most attention.

What Happens When Due Diligence Expires?

Ideally, you wrap up due diligence and the buyer decides whether to go forward with the purchase. If you don’t complete the process on schedule, you have a couple of options: You can either extend the due diligence period until you complete the process or move on without completing the deal.

Due Diligence M&A Checklists

Due Diligence M&A Checklists

In this section, you’ll find a variety of free, downloadable checklists for various aspects of the due diligence process. These checklists strive to cover mergers and acquisitions in general, but they may not include some documents and information that are specific to particular fields, and others that may not apply to all deals. Buyers should review the lists and add or delete items as needed.

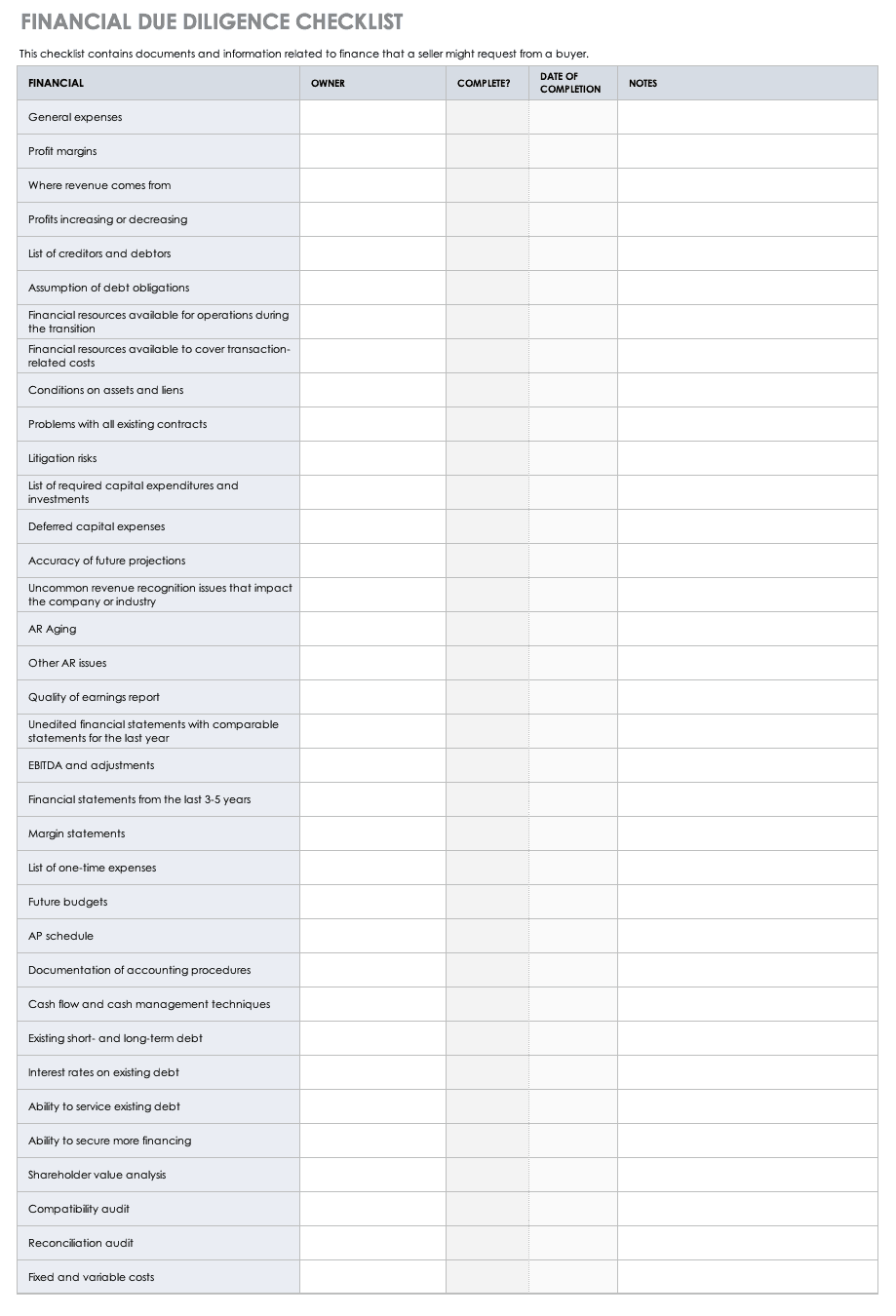

Financial Due Diligence Checklist

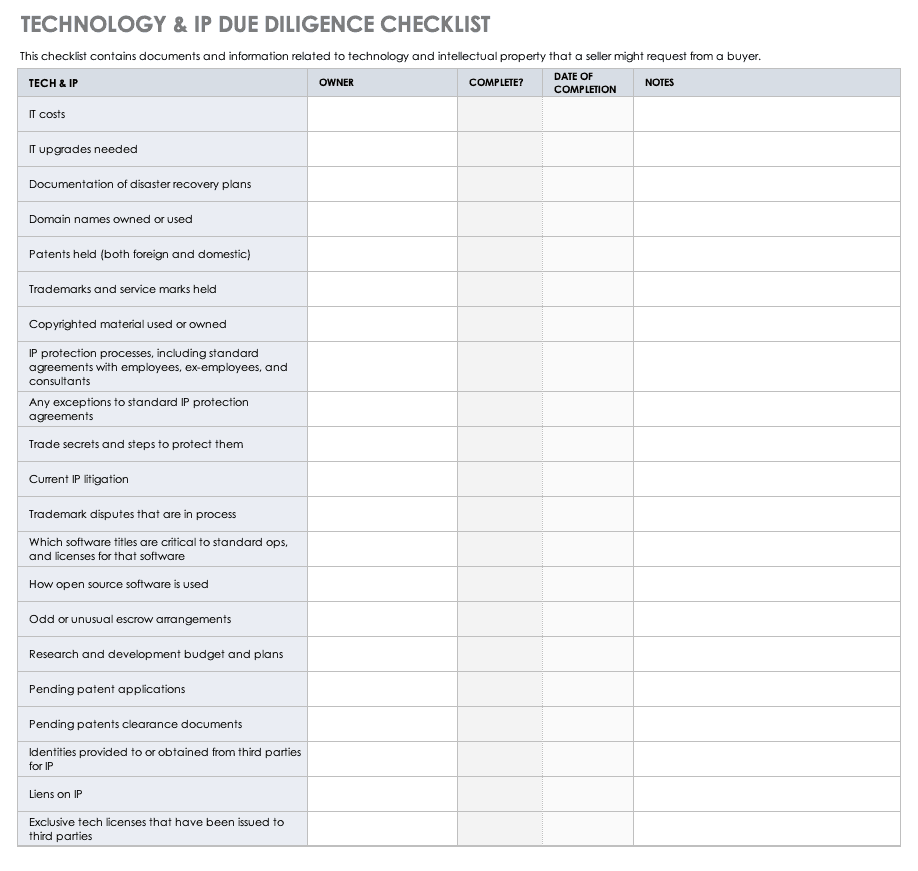

Technology and IP Due Diligence Checklist

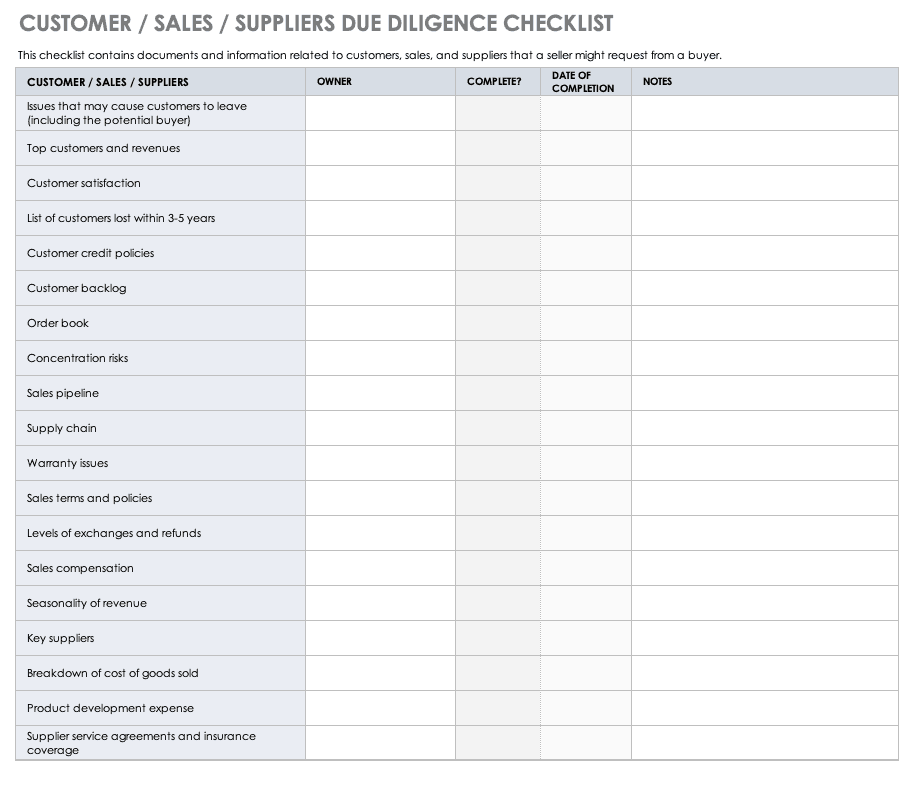

Customer/Sales/Suppliers Due Diligence Checklist

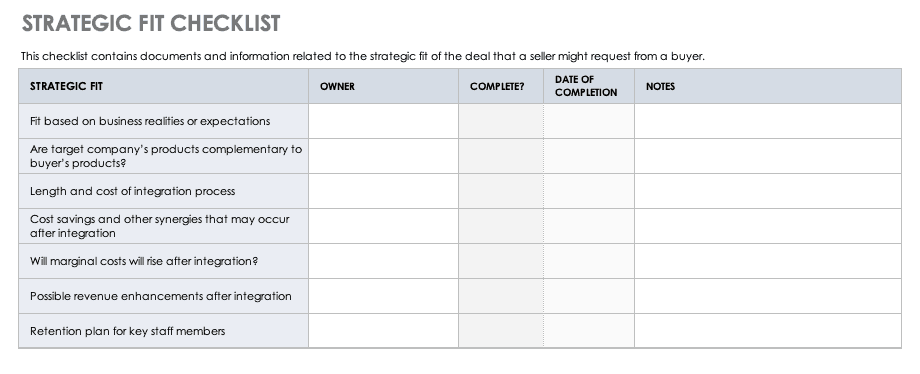

Strategic Fit Checklist

Material Contracts Due Diligence Checklist

Employment/Management Due Diligence Checklist

Litigation/Legal Due Diligence Checklist

Taxes Due Diligence Checklist

Antitrust and Regulatory Due Diligence Checklist

Insurance Due Diligence Checklist

General Corporate Matters Checklist

Environmental Issues Checklist

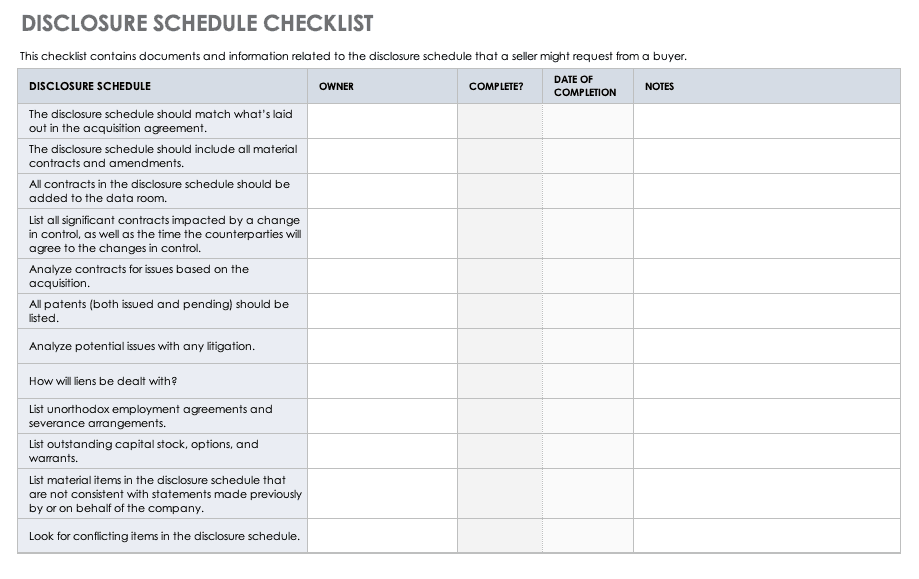

Related Party Transactions Checklist

This checklist contains documents and information addressing related party transactions that a seller might request from a buyer. These checklists strive to cover mergers and acquisitions in general, but they may not include some documents and information that are specific to particular fields, and others that may not apply to all deals. Buyers should review the list and add or delete as needed.

Download Related Party Transactions Checklist

Property Due Diligence Checklist

Marketing Due Diligence Checklist

Competitive Landscape Due Diligence Checklist

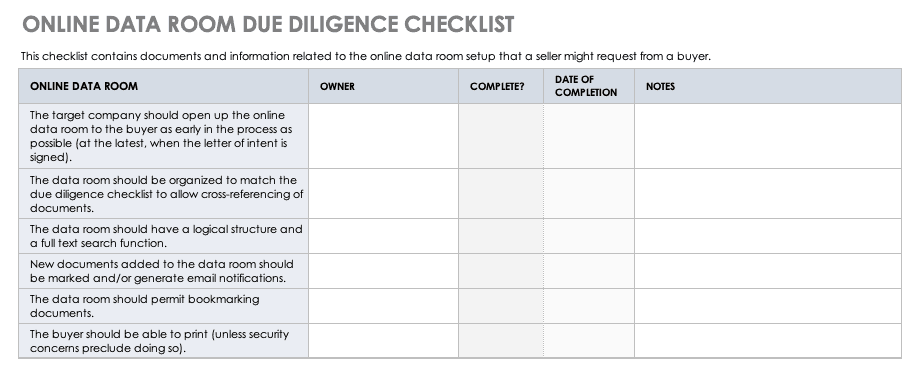

Online Data Room Due Diligence Checklist

Master Due Diligence with Real-Time Work Management in Smartsheet

Empower your people to go above and beyond with a flexible platform designed to match the needs of your team — and adapt as those needs change.

The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

When teams have clarity into the work getting done, there’s no telling how much more they can accomplish in the same amount of time. Try Smartsheet for free, today.