What is a Balanced Scorecard?

A balanced scorecard (BSC) is a management tool used for strategic planning. Generally speaking, a BSC is a standardized report that details performance management measures. With a BSC, you have the ability to describe and measure your company strategy and then track how you achieve results. This is a big-picture view with lower-level, specific, defined measures to attain that big picture. Instead of gauging how well your company is doing based on how much revenue is coming in in the short term, a BSC helps you build a sustainable business for the long haul - by doing so, the BSC gives you a truly “balanced” picture of your company. You will design your BSC when you have already developed at least part of your company strategy, but a BSC does not create your company strategy for you. However, it can help if you’ve only partially completed your strategy, because it can reveal the inconsistencies and holes in your team’s initial thinking. In addition, a BSC reports not only financial performance measures but also nonfinancial performance measures.

The BSC framework itself is based upon leading and lagging indicators. Leading indicators are drivers - those that help you look ahead toward achieving your goal - and should be predictive in nature. By contrast, lagging indicators are outcomes - those that tell you what has already happened - and should confirm your long-term trends. A good BSC has a healthy mix of leading and lagging indicators.

To measure outcomes, you’ll use key performance indicators (KPIs), the metrics that show whether your company is achieving what it set out to do. Some examples of leading indicators are the number of new innovations, the growth in new markets, and the number of patents. Some examples of lagging indicators are revenue growth, earnings before interest, tax, depreciation, and amortization (EBITDA), and operating income growth. However, regardless of the indicators you choose, there should only be a small number per scorecard so you can focus your efforts.

The Four Perspectives of the Balanced Scorecard

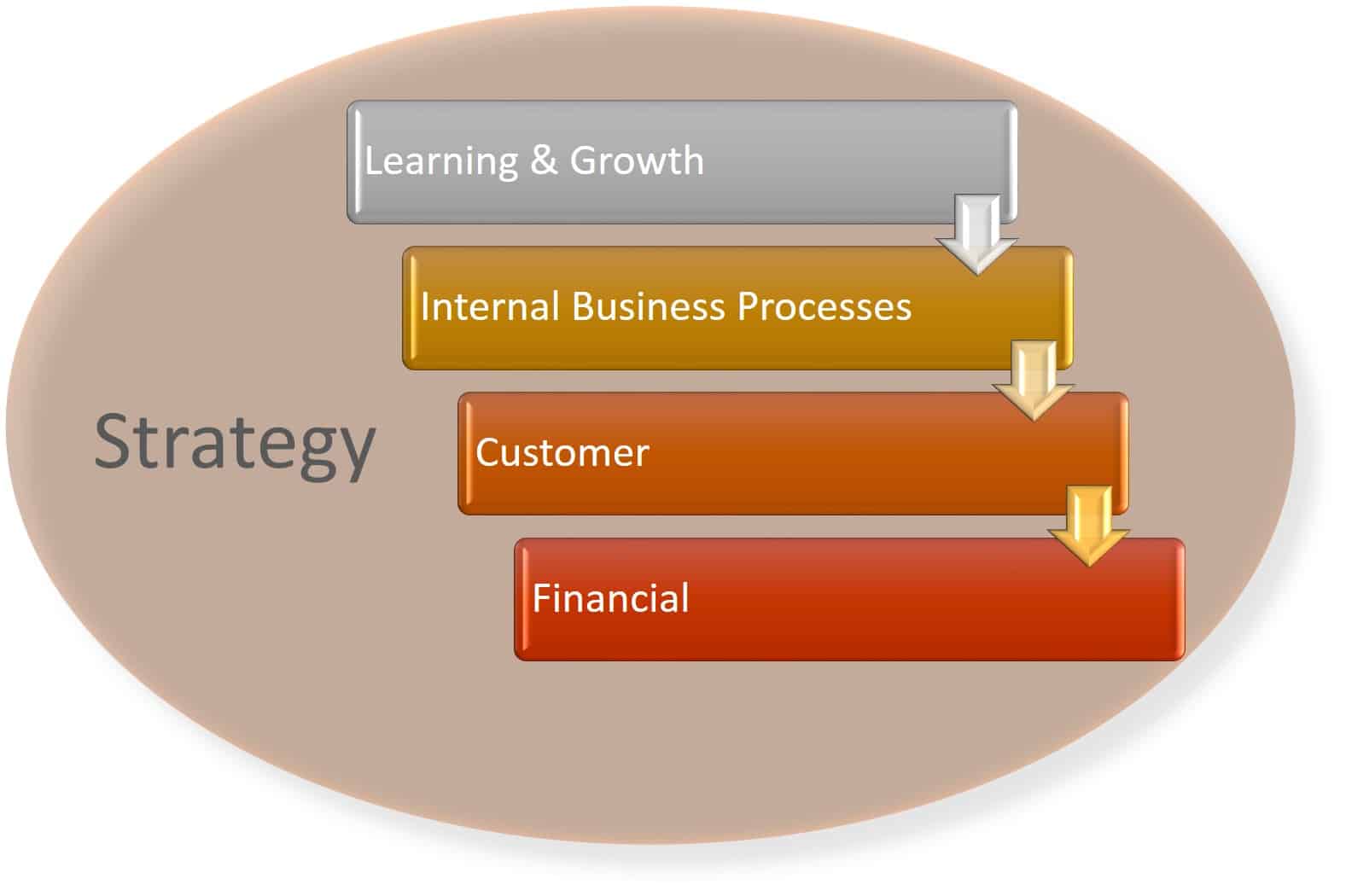

The BSC breaks your business down into four different perspectives that measure your company’s condition. These perspectives are often called four legs. The four legs concept posits that each leg is equally important - losing one would render a whole business unstable. Each leg symbolizes a different group of stakeholders to whom your company is responsible. These stakeholders consist of the following groups: financial, internal business processes, the customer, and learning and growth. These perspectives are dependent on each other and build from your culture of sharing and development to the financial health of your company.

- Learning and Growth: This perspective focuses on the people, information, and organization and how you can improve upon and create more value in these elements. This category also refers to your company’s ability to constantly improve, innovate, learn, and be competitive. The remaining three perspectives grow out of this leg.

- Internal Business Processes: When we look at this perspective, we are really asking, What must we excel at? In order to please our customers and stakeholders, we must first implement processes that enable us to do so. Further, we should optimize these processes to improve quality and efficiency. Process data can show you exactly where any problems with the product or service lie.

- Customer: Your customers’ perception of how your company is performing is the key to keeping it alive. Management should focus on the specific measures to please customers, rather than the strategic goal of pleasing customers. These specific measures should fall into five categories: timeliness, quality, performance, service, and cost.

- Financial: This perspective covers the revenue or financial performance of your company (i.e., what your shareholders see). You outline your profit targets, budget, and cost-saving measures in this perspective. The performance of this perspective is usually strong when the other three perspectives are strong.

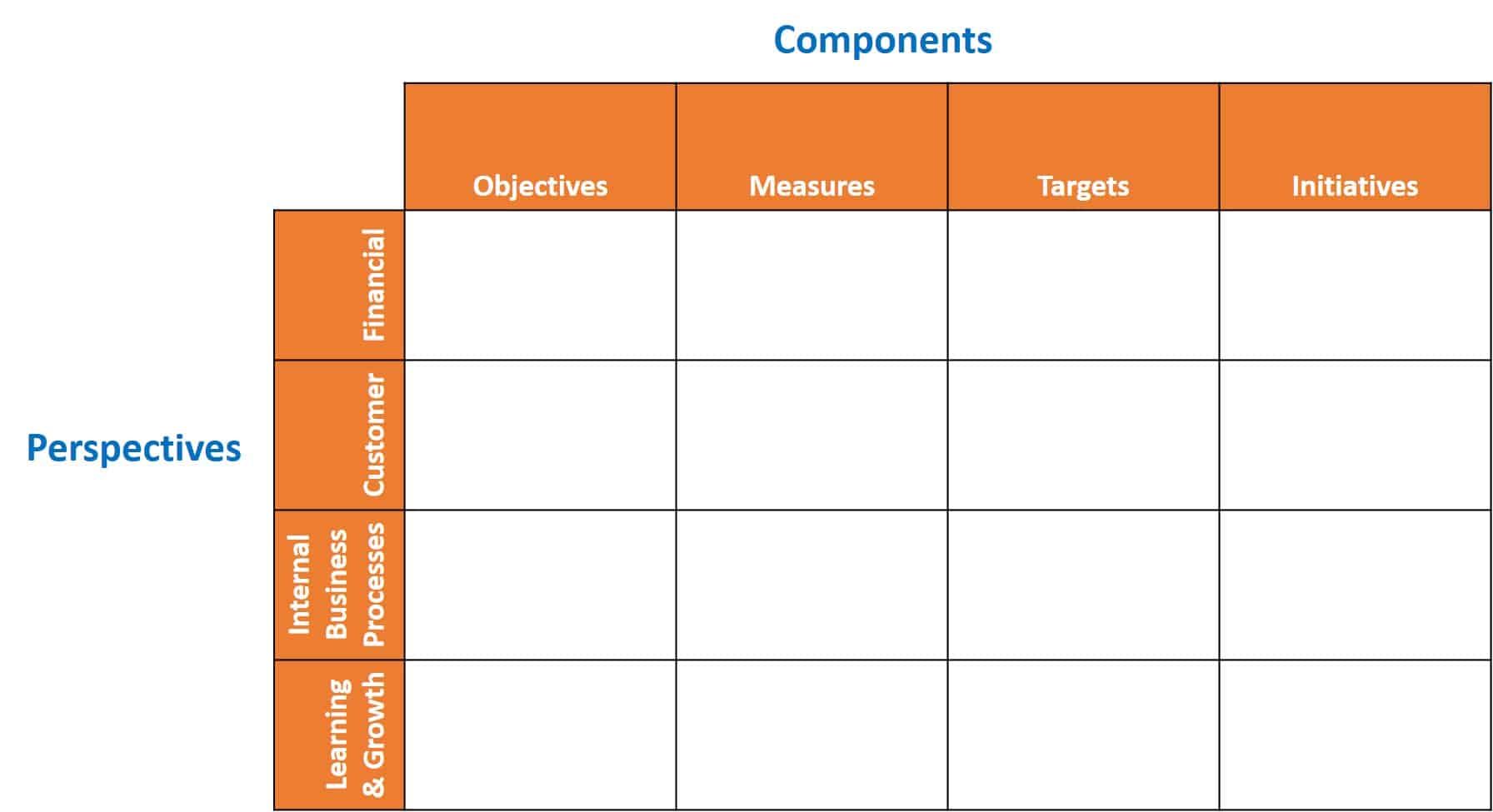

The Components of the Balanced Scorecard

For each perspective, there are four main BSC components that you must define:

- Objectives: These are your high-level organizational goals. Taking into account your already-developed company strategy, you should be able to come up with 10-15 strategic objectives that you are trying to accomplish. You can use a SWOT analysis to define these objectives. (The SWOT is a review of your business’s strengths and weaknesses, opportunities, and threats.) Your objectives should be S.M.A.R.T.: specific, measureable, achievable, realistic, and time-specific.

- Measures: After you define your business’ objectives, you need to focus on its measures. The measures help you determine whether you are on track to achieve your objectives (you can think of measures as KPIs). Each objective should have no more than three KPIs that indicate whether you will achieve your objective. Strong KPIs should be objective enough for you to determine whether the strategy is working, use language that everyone in your company understands, measure accomplishments, show success (not just a useless metric), be able to show change over time, and reduce uncertainty.

- Targets: You should write your targets so that they relate directly to each of your KPIs. For each KPI, you should have an associated value. Your targets should be ambitious but achievable.

- Initiatives: In your BSC framework, your initiatives should be the action items and projects that you need to help your company succeed with its strategy. These projects have a start and end date. You should identify them when writing your BSC and set them up when implementing your BSC. Your initiatives mean the difference between your company’s reality and its stretch targets.

Your scorecards can take on many shapes and designs, so you have the leeway to design a scorecard that reflects your unique company culture. You may also want to amend it to address the specific population that you’re serving. For example, a government organization serves customers, not citizens. You can simply adjust your wording to customize your scorecard. In addition, you may want to include your company logo and colors. A blank scorecard could look like this to start:

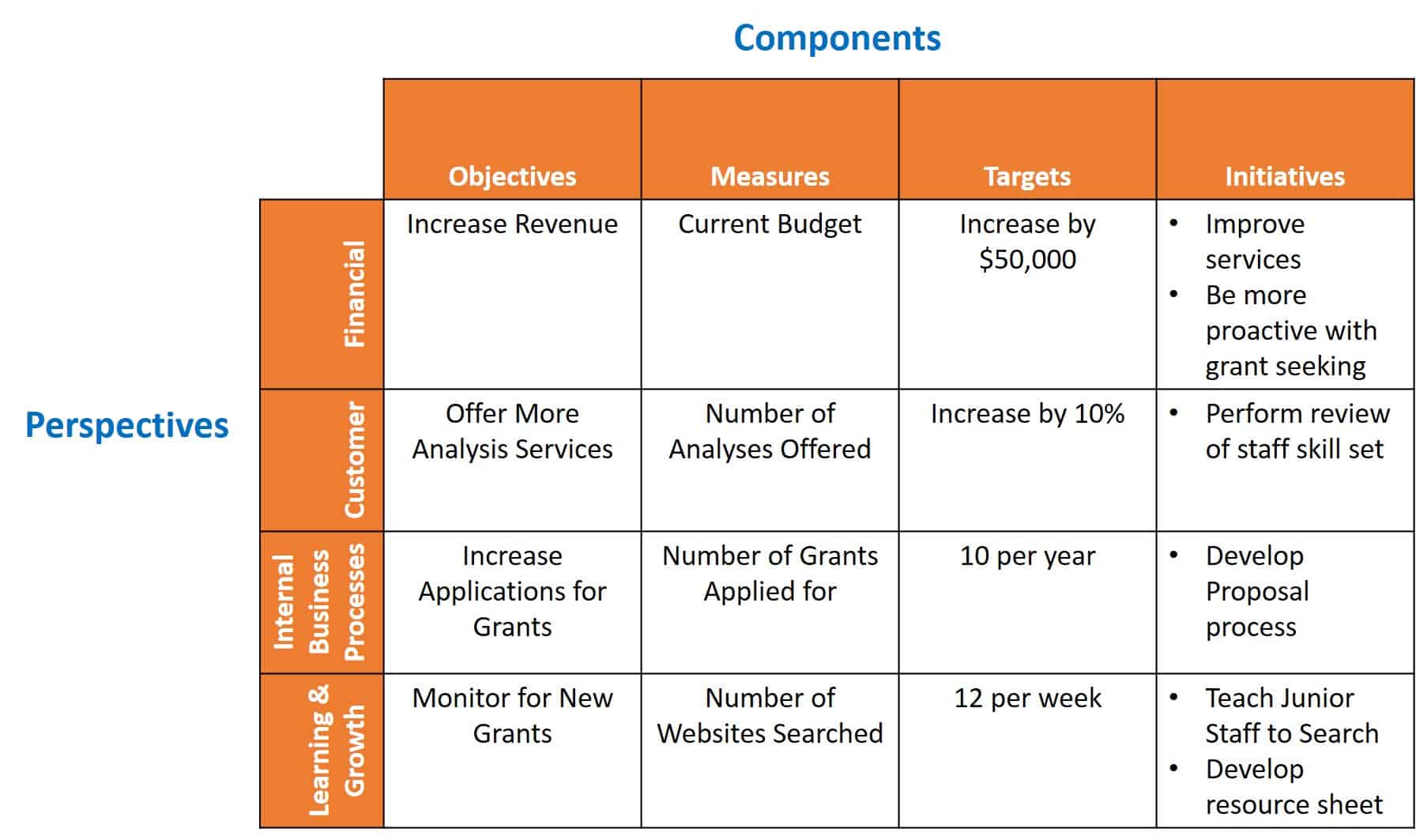

Here is an example of what a scorecard for a research company might look like:

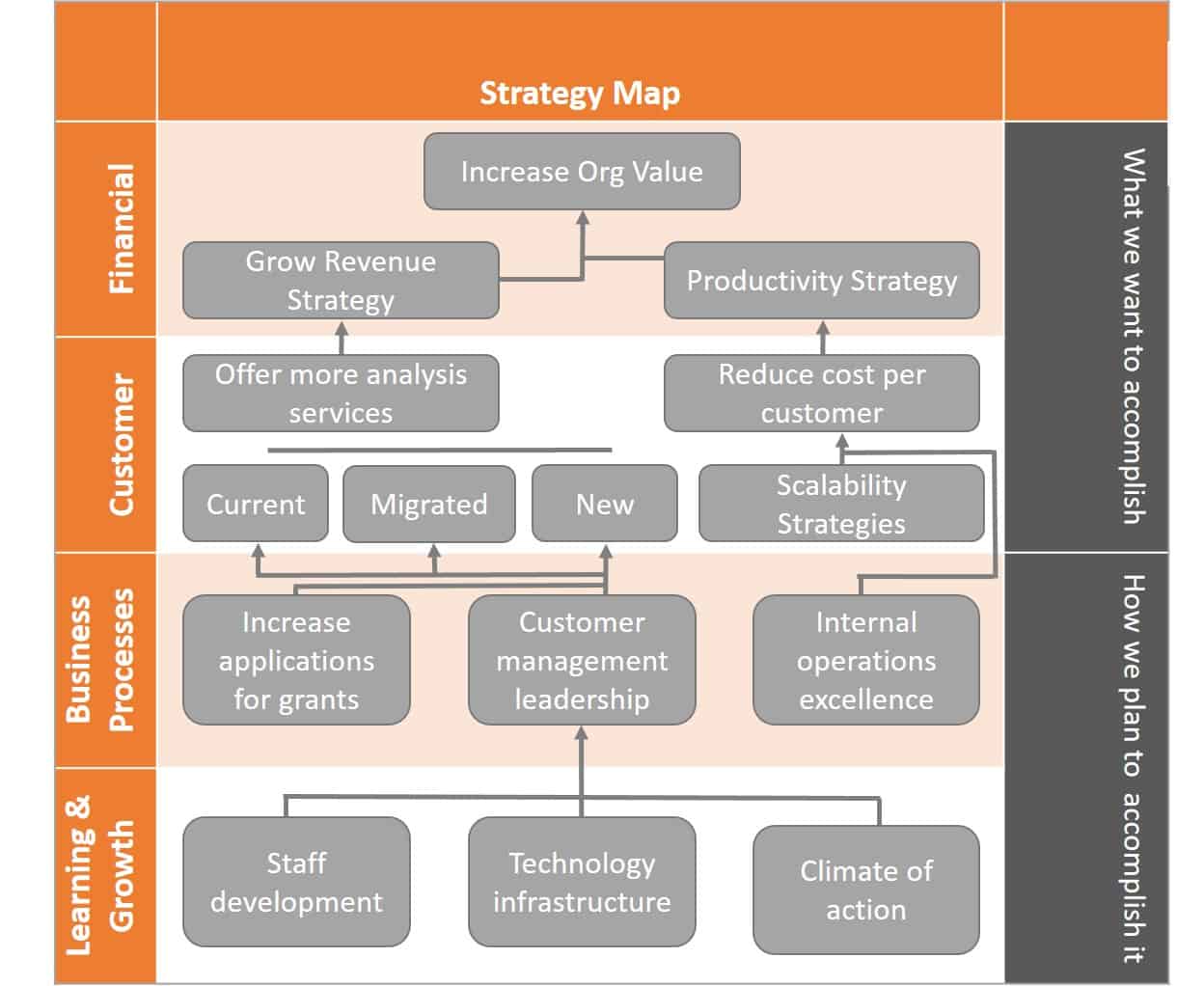

The Purpose of a Strategy Map vs. a Balanced Scorecard

Many experts feel that a strategy map is just as important as a BSC (if not more so) in certain situations. Created by the same experts who created the BSC, a strategy map shows your company’s strategy-linked objectives. The difference between a BSC and a strategy map is that the strategy map shows the cause-and-effect relationship between the perspectives and the components. Together, the strategy map and the BSC help your company successfully execute your strategy. The two also speak to what you want to accomplish and how you plan to accomplish it. You can also use a strategy map on its own. The benefits of strategy maps include the ability to:

- Effectively capture and communicate your strategy

- Manage your team’s performance better

- Pinpoint your company’s focus, drivers, and choices

- Create a better BSC

- Take your focus from operations to strategy

Some experts recommend that you design your strategy map before you complete your scorecard. The ideal time to fill in the strategy map is after you have determined your BSC objectives but before you’ve filled in the measures. The same four balanced scorecard perspectives apply to the strategy map (financial, customer, internal business processes, and learning and growth). The primary difference here is that with a strategy map, you show the direction (causal relationships). For example, we could expand a portion of our earlier balanced scorecard for the research firm:

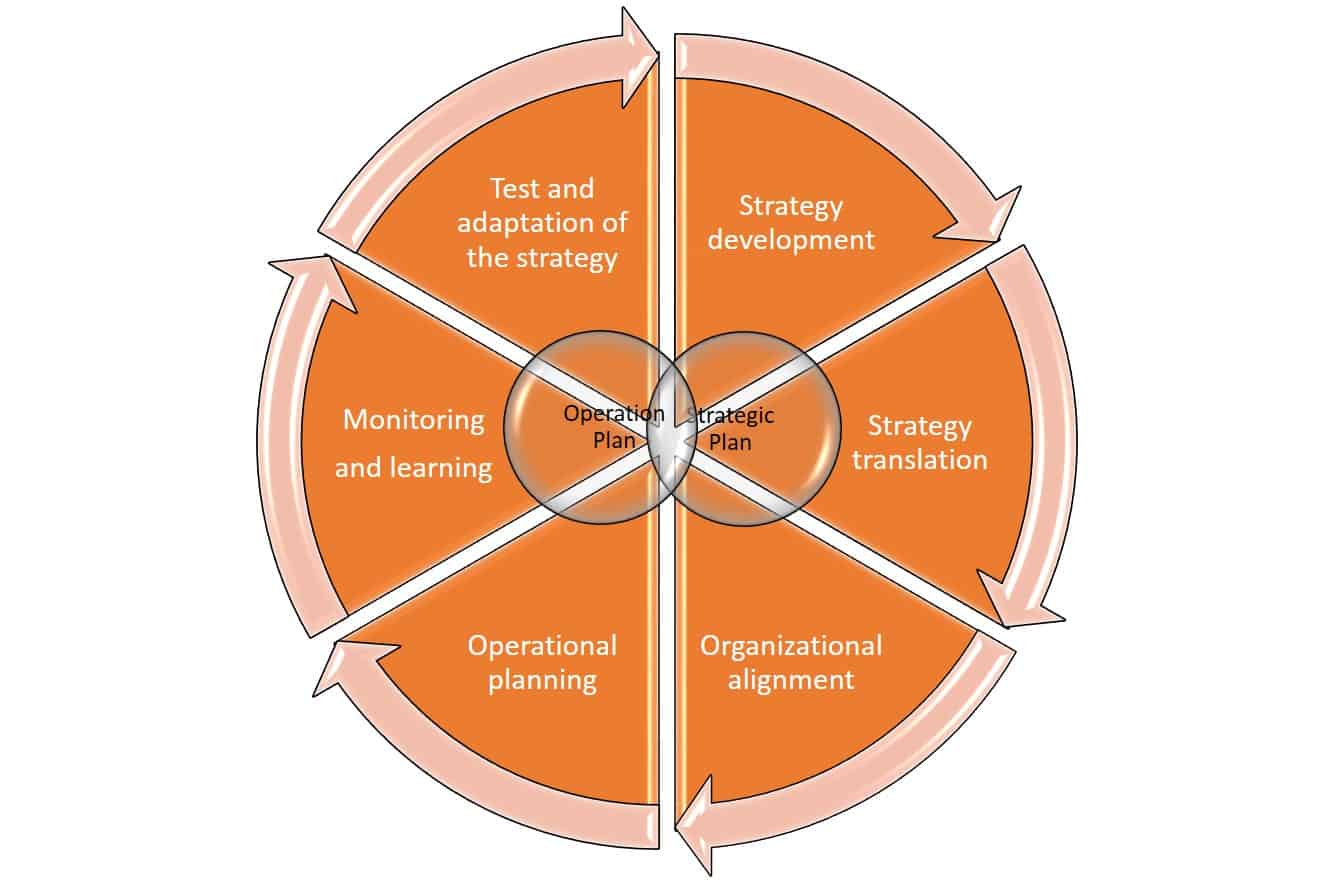

The Balanced Scorecard in a Closed-Loop Management System

A closed-loop management system is a structure that uses feedback from the ongoing operations to improve processes. This feedback could be information from the same or from a different area of the value chain - either way, it helps to improve processes earlier in the loop. The system includes six stages:

- Strategy development

- Strategy translation

- Organizational alignment

- Operational planning

- Monitoring and learning

- Testing and adaptation of the strategy

Robert S. Kaplan, co-creator of the balanced scorecard and Senior Fellow, Marvin Bower Professor of Leadership Development, Emeritus at the Harvard Business School, discuss using this closed-loop management system together with your company’s strategic planning and operations execution as a complement to the BSC. In other words, the closed-loop system constantly improves upon the strategic plan and the operating plan. As the BSC is a part of the management system, it continually improves upon that as well.

The History of the Balanced Scorecard

Experts consider the concept of the BSC in professional organizations one of the most significant management ideas of the past 75 years. First introduced in the early 1990s by Kaplan and David P. Norton (also of the Harvard Business School), professional organizations around the world use it today. The difference between the scorecard and other tracking mechanisms is that it combines financial and nonfinancial measures, where traditional measurers only track financial measures.

The first generation of the BSC was a 4 box approach. The four boxes included the same categories that they do now (financial, customer, internal business processes, and learning and growth). However, instead of possessing four components, this inaugural version of BSC simply recorded goals and measures for each perspective. This first generation showed causality, but organizations did not use the causality for any specific purpose. Many organizations still use first-generation scorecards as their model.

Second-generation BSCs evolved because some professionals felt that the first-generation BSC descriptions were too vague and the interpretations too liberal. The changes were small but amounted to a new definition of a BSC. The authors added a more process-oriented method to determine the key measures. From the goals and measures recorded for each perspective, the authors added strategic objectives to better align with businesses’ own strategies. Finally, the authors added definite causal linkages between each perspective and component.

The third-generation BSC was developed in the late 1990s., and is distinguished from the previous versions by its components and the design process. The new components of the third-generation BSC include a vision statement, definitions for the strategic objectives, targets for the measures, and the strategy map to go along with it, and the design process requires involvement from the company management. This is to ensure that the strategic objectives are cohesive and take primacy.

Since the third generation was introduced, the concept has been expanded for nonprofit and public-sector entities, strategy and operations have been linked in a closed-loop management system, and strategy management has been developed.

The Future of the Balanced Scorecard

The biggest factor for the success or failure of a company’s BSC is always the leadership. Therefore, many BSC experts believe that the future will bring more research on what makes good leaders. Good leadership not only supports and grants buy-in on the development of the BSC, but also acts as its cheerleader, pushing its strategic objectives.

Although the ability to evolve with modern management concepts has kept the BSC relevant, experts have suggested certain changes that may or may not be appropriate to your company’s particular makeup. One of these includes using predictive analytics alongside the BSC. Predictive analytics detect future trends in business and help leaders determine what KPIs can collect useful data.

Ultimately, though, most of the experts say that the future of the BSC is based upon the individual industries: as industries evolve, so will their scorecards. For example, in the energy sector, the scorecards will look increasingly at more sustainable objectives. In the technology industry, the objectives on the BSC will include those more commonly seen in other industries. This will reflect the convergence of multiple industries and the concept of technology convergence.

The Popularity of the Balanced Scorecard

Even in its early iterations in the 1990s, the BSC was unsurpassed as a management tool. Today, remarkably, it is still the most popular performance management tool in companies worldwide, according to experts Darrell Rigby and Barbara Bilodeau. There are many different iterations of the BSC on the web. However, the purpose of the BSC is not just to fill in the blanks and post a piece of paper on the wall; rather, the BSC is a development process for your company. Designing it and filling it in is an exercise in evolving your business strategy. The early failures of the BSC were due to consultants who filled them in without insider business knowledge and stake. The beauty of the BSC is that it ties directly to strategy execution to align everyone in your company, provides transparency into company intent, and adapts to your business.

Information Technology and the Balanced Scorecard

Over the last few decades, Information Technology (IT) professionals have realized that a company’s IT strategy and business strategy must be aligned. We normally track five types of IT metrics on a company’s BSC. These metrics include:

- Financial Performance: This category reflects the spending on IT projects and service.

- Project Performance: This category looks for new funding streams from IT development projects and savings from IT improvements.

- Operational Performance: This category measures the higher-level view of IT operations, such as availability and outage length. It is not concerned with daily performance.

- Talent Management: This metric category evaluates how attractive the department is to new talent and how satisfied current IT staff are with their positions.

- User Satisfaction: This category analyzes the user perspective, including how the customers of the IT department (such as the rest of the company) rate the department’s performance.

In the four perspectives, this translates to the following:

- Financial: Design metrics that show how IT optimizes its efficiency and how it enhances its impact on the business’ outcomes

- Customer: Design metrics that show quality service and give the business innovative solutions

- IT Internal Business Processes: Design metrics that show how IT maintains a reliable infrastructure, gives an effective support system, and offers and delivers transformative applications

- Learning and Growth: Design metrics that show how IT promotes a customer-focused culture, enhances its staff experience, and develops the IT staff competencies

Human Resources and the Balanced Scorecard

Human resources (HR) is another key department that you should align with the overall company strategy. HR scorecards should focus on leading indicators. In this way, you can bring in the staff you need and plan for the future of your company. Your HR scorecard should also identify what is doable vs. what is deliverable. The HR BSC follows much the same path as the overall company BSC since HR is a higher-level function within any organization. It should also utilize the same four perspectives:

- Financial: The metrics for HR should delineate return on investment (ROI), such as the cost per hire, the value-add per employee, and the cost of recruiting.

- Customer: In the context of HR, this means the company’s employees and the potential employees. This set of metrics should look at how you are increasing the attractiveness of the company. This includes how satisfied your employees are, how many applications your company receives, how many applicants you reject, and how well the recruiting process works.

- HR Processes: This is the row on the HR BSC that may look different from that on the traditional BSC. This section focuses mainly on how your business is improving its culture, how you are developing and retaining staff, and how you are attracting quality candidates.

- Learning and Growth: For these metrics, you are looking at how you are developing your workforce, the techniques and training that can help you improve your processes, and whether there are technology purchases you should make to stay competitive.

Accounting and the Balanced Scorecard

Accounting firms are service-based organizations. Just like other service-based firms, they should analyze their operating goals and strategies on a regular basis to ensure that these two elements are moving in an intentional direction. However, in choosing metrics for their BSC, accounting firms should make sure the four perspectives deliver accounting-specific metrics to gauge their performance. For the four perspectives in this case, the metrics to consider during development are as follows:

- Financial: The metrics for accounting should consider your firm’s objectives and implement the tangible financial outcomes of your strategy. These may include fee revenues, professional salaries, margins, and reduced receivables.

- Customer: This perspective should illustrate the way that your firm would satisfy its customers. Customers of accounting firms are generally looking for short job turnaround time and work well done. Your metrics can convey the status of these factors through the number of client complaints, referrals, and contacts per period.

- Internal Business Processes: Most of your accounting firm’s internal processes are administrative. These may include metrics on the number of profitable projects, the new software you’ve implemented, the bidding estimates you’ve accepted, and utilization rates.

- Learning and Growth: In accounting firms, your HR department is your biggest asset in developing your workforce. It can help you develop workforce plans to keep your staff up to date and competitive.

Who Develops and Uses a Balanced Scorecard?

Nonprofit and government industries were not able to use the early iterations of the BSC because those early versions were specific to customer-oriented industries. Now, any industry of any size can and should use the BSC. Even technology giant Apple, Inc. and the U.S. Government Office of Personnel Management (OPM) use the balanced scorecard approach. According to the Harvard Business Review, Apple’s five performance indicators are as follows:

- Customer satisfaction

- Core competencies

- Employee commitment and alignment

- Market share

- Shareholder value

High-level executive or division leadership teams should drive scorecard development. Without leadership buy-in, balanced scorecards will fail. Leaders should integrate strategic management approaches into their scorecards. Experts recommend a three-team approach for developing BSCs enterprise-wide. Each team should have specific experiences and competencies, and include people from the following groups:

- Upper-Level Management: Managers on this team should be strategic thinkers and have an overall understanding of the business. They should also be excellent communicators and able to make strategic business decisions. This is your general leadership team, sometimes known as executive sponsors.

- Mid-Level Management: Managers on this team should also be good communicators and well educated in the business. Additionally, it’s vital that employees respect these mid-level managers, as they will be the ones championing the BSC throughout the company. Lastly, they should be detail-oriented yet able to see the big picture. This team is your core team.

- Lower-Level Personnel: This team is capable of linking the material from the two other teams to their specific job functions. They should have a highly detailed understanding of these jobs and be able to come up with detailed metrics. This team is the measurement team.

The Balanced Scorecard Automation and Performance Analysis

Once you fill in your scorecard, there are many options for tracking including pen and paper, BSC-specific software, and generalized tools. The BSC was developed to be a performance management system. Many experts recommend that once you build your scorecard, you should automate it. This means finding performance management software that’s right for your company, or making use of software that you already have. The software takes your innovative BSC ideas and implements them evenly throughout your company. Many software packages can handle not only the BSC, but the strategic mapping as well. In bigger enterprises with multiple BSCs — one for the overall strategy and one for each division — software is a good way to keep them organized. Moreover, the software can help you coordinate the development, production, and distribution components across the entire company.

There are some benefits to automating your BSC with Microsoft Office products, such as Excel or PowerPoint. Most of your professional staff will already be comfortable working with these programs, so they can easily customize the software to the company’s needs. However, managing multiple documents from one reporting period to another may take some creativity, as that particular feature is not inherent in these programs. Furthermore, Microsoft products do not address the issue of version control, so you may have multiple iterations of your scorecards floating around between all of your users.

There are applications that cater specifically to the BSC, so you don’t need to customize or program them. These apps can also manage multiple users, providing version control and tracking updates. And, they can generate the BSC-related reports and analytics that you need. Nevertheless, sometimes they are too specific and cannot be linked with your other business applications. Also, not all of these programs are intuitive, which can lead to the added expense of staff training. This is, of course, in addition to the cost of the software.

Another option is a Business Intelligence (BI) solution. BI solutions are categories of software designed to analyze business data, not just collect it. This software captures your automated processes, and can generate real-time analytics. The upside of this type of software is that your data warehouse of analytics systems is probably already working with a BI solution. Therefore, you can store all of your data in one location. The downside of a BI platform is that your average user is not familiar with it (which again leads to the additional expense of outside experts). What’s more, BI reports for high-level staff are not easy to generate and typically do not include anecdotal or qualitative information.

The Balanced Scorecard Benefits and Strategy

The biggest benefit of the BSC is that it brings together all of the disparate elements of your company tactics into one report. Since all the operational metrics are in one place, your executive management can see the sacrifices linked to each improvement. Other benefits include:

- Taking a vision and making it a reality

- Improving transparency within the company

- Ensuring your company has strategic priorities

- Making decisions using real-time data

- Managing the environment more effectively

You should build your BSCs in a cascading manner. This means that you are translating your overall corporate scorecard down the line to lower levels. This results in a clear strategy from top to bottom. As you descend the levels of your organization, your BSCs will reflect more operational and tactical, and less strategic, measures.

Building a BSC can be a challenging but worthwhile venture. You will start by prepping all of your materials, including your current strategic plans, financial plans, marketing plans, operating plans, annual reports, quality improvement programs, and customer analyses. You should also interview your executive management team repeatedly for their ideas (do this before you develop your BSC and as you get closer to completing it). Other sources of information should come from your industry’s competitive analyses, trend analyses, technology trend analyses, and marketing trend analyses. Once your team has gathered all the necessary information, they can follow the steps to design your BSC. We’ve already covered most of the steps, but their sequence is outlined below:

- Identify your company’s vision and mission.

- Develop a strategy with a customer-first lens.

- Develop objectives that expand on your mission statement.

- Perform your strategic mapping.

- Develop your performance measures.

- Develop projects that initiate performance accountability.

- Come up with a system to track your objectives and initiatives and report on them.

- Ensure your BSC’s cascade.

- Perform an after-action review of your process.

- Adjust your BSC regularly, based on your closed-loop feedback.

The following are our expert’s tips for managers new to developing BSCs.

Robert Key, Senior Project Manager and Agile Coach, AMN Healthcare

Here’s what Key had to say about developing BSCs:

“My experience with the balanced scorecard comes from working as a project manager and Agile coach and teaching at the University of Phoenix and the University of San Diego. I have helped put together balanced scorecards for many different teams and taught strategic management courses. The main industries that I have focused on are education and healthcare recruiting.

“I often talk about a cartoon that I once saw. It was a CFO talking with a CEO. The CEO asks, ‘But what happens if we train them and they leave?’ when discussing their workforce. The sage CFO replies, ‘What happens if we don’t and they stay?’ To me this illustrates perfectly the importance of not ignoring the training and education piece of the scorecard (the learning and growth perspective). Many in management are fixated on the other quadrants, but managers, especially new managers, need to learn the value of training and educating their people. This is a cost center, but what happens when you remove training is that the morale crumbles. In lean financial times, this is usually the first thing cut. However, this defeats the purpose and does not save any money. This is the equivalent of stabbing yourself in the foot. In particular, new personnel who come in do so at a disadvantage, putting your whole organization at a disadvantage.

“If I had to advise managers new to the balanced scorecard, I would tell them to use Six Sigma techniques during design as needed, especially when developing the internal business process and customer sections. If you do the other three right, the finance part should follow easily. Choose executives carefully: your CFO and VP of Human Resources for your education section, your sales leaders and high-level reps for your business processes, and even IT for the customer section. Speak with anyone who faces and interacts with your customers, looking to get different scenarios and input on how we can work better. Consider performing surveys.

Regarding the finance piece of the equation, if you do everything else right, finance should follow.

“I have really worked, even volunteered on my own time, to ensure that our workforce learns what they need to in order to be successful. I love to teach, and this comes out in all of the places that I work. It is because I have been so fortunate: I had amazing teachers who taught me the value of giving back. I have even hosted ‘lunch and learn’ sessions.

“Finally, you should not avoid any of the quadrants. You may not know the answers, but, if that is the case, you should seek input from other departments or resources. Don’t make it up on your own unless you know what you are doing and avoid external consultants. Internal consultants, if available, are your best bet because they know your business. If you must use an external consultant, use them for benchmarking after your analysis is completed.”

Learn More About the Balanced Scorecard

The BSC was developed in the early 1990s. Since then, a multitude of resources has become available to show you how to develop your own BSC and put it to work for your company. However, the best resources are still the books by the original authors of the BSC. By reading and referencing these books, you can truly understand the design process as it was meant to be and achieve the best results for your company. These books include:

The Balanced Scorecard: Translating Strategy into Action, Kaplan and Norton, 1996.

The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment, Kaplan and Norton, 2000.

The Execution Premium: Linking Strategy to Operations for Competitive Advantage, Kaplan and Norton, 2008.

Strategy Maps: Converting Intangible Assets into Tangible Outcomes, Kaplan and Norton, 2003.

For nonprofits and government agencies, check out the following book on the BSC: Balanced Scorecard: Step-by-Step for Government and Nonprofit Agencies, Niven, 2003.

Use Smartsheet to Gain Actionable Business Intelligence

Empower your people to go above and beyond with a flexible platform designed to match the needs of your team — and adapt as those needs change.

The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

When teams have clarity into the work getting done, there’s no telling how much more they can accomplish in the same amount of time. Try Smartsheet for free, today.