Projects face many different types of risks, from scope creep to system failures and external disruptions. Understanding the various categories of project risk will help you identify, measure, and prepare for potential threats before they derail your next project.

Risk categories are high-level groupings of project risks, organized by source or type. In project management, risk categories are typically arranged in a risk breakdown structure (RBS), where broad sources of uncertainty — such as technical, financial, organizational, or external risks — are subdivided into more specific risk types.

One common method is to distinguish between project-level and business-level risks. Project-level risks have the potential to affect results at the project level, while business-level risks have the potential to affect the overall operations of a business.

The following diagram is an example of how risks may be further broken down into additional categories:

No matter how risks are categorized in the RBS, successful project risk management begins with well-trained project leaders who can recognize and respond to threats across categories. Learn more about the basics of project risks in this comprehensive guide.

“The risks you might encounter can vary greatly, but the greatest risks each company faces are the actions of the people in project authority. Their training and attention to planning a project completely and executing according to the company processes is the cornerstone for success.”

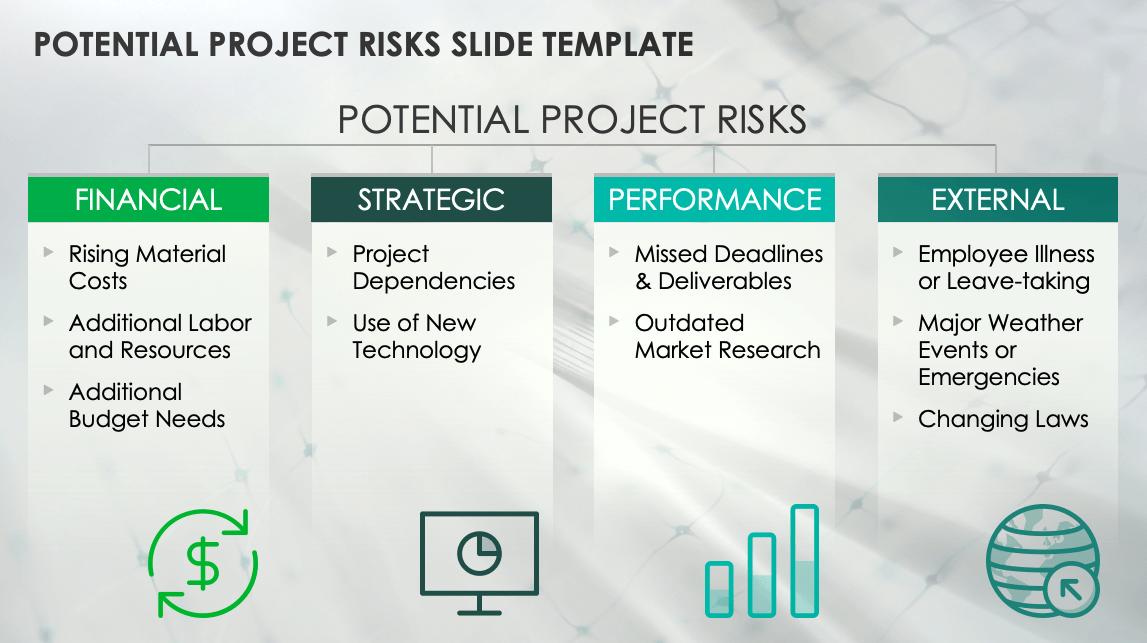

Include this template in your next presentation to help identify and communicate key project risks. The template organizes risks into four categories: financial, strategic, performance, and external. It comes partially prefilled with sample text to help you get started. Customize it to reflect the risk categories that are most relevant to your project.

Find other risk management tools, like a risk assessment matrix and a risk assessment questionnaire, in this collection of project risk templates.

10 Common Types of Project Risk

The 10 most common types of project risk include technical, financial, operational, external, organizational, and strategic risks. Scheduling, scope-related, resource-based, and stakeholder risks are also common. These categories cover the primary ways projects can fail. Understanding these risk categories helps teams identify the most likely and impactful threats.

Here are the 10 most common project risk types:

1. Technical Risks

Technical risk, or technology risk, is the possibility that a technology, design, or engineering solution will not function as intended.

For example, a tech company might launch a project to build a mobile app using a new authentication framework. Imagine that midway through development, the team discovers that this framework cannot integrate with existing systems, forcing a redesign that delays the release and increases costs. The team could have mitigated this risk by conducting a proof of concept before full development.

Technical risks can stem from reliance on unstable third-party components, technical skill gaps, or poor due diligence. Addressing these factors early helps reduce the likelihood of late-stage redesigns and system failures.

Common Causes of Technical Risks:

Use of unproven or immature technology

Complex system integrations

Unclear or incomplete technical requirements

Inadequate testing or quality assurance

How to Mitigate Technical Risks:

Validate technical feasibility early

Define and document technical requirements

Conduct thorough system integration planning and testing

Engage subject matter experts for architecture and design decisions

To learn more about mitigating technical and other types of risks, see this guide to effective project risk mitigation.

2. Schedule Risks

Schedule risk, or timeline risk, is the possibility that project activities will take longer than planned. Schedule delays can cascade through a project, causing missed milestones and deadlines.

For example, a software company might schedule a new feature release in three months but underestimate third-party API integration complexity. If the third-party provider does not deliver the required materials on time, developers cannot properly test or build the integration. The launch would have to be rescheduled, extending the timeline and frustrating customers.

Schedule risk can arise from resource constraints, unmanaged task dependencies, and mid-project scope changes, among other factors. Delays from vendors and required rework can also cause delays. Regular schedule reviews and proactive dependency management help teams identify and address risks before they affect delivery dates.

Common Causes of Schedule Risks:

Inadequate project planning

Inaccurate or overly optimistic time estimates

How to Prevent or Mitigate Schedule Delays:

Build buffer time into project schedules

Use the critical path method to identify potential bottlenecks

Track actual versus estimated time

Implement daily standups for early issue detection

Leverage Gantt charts with dependency tracking for timeline visibility

Learn to identify and prioritize potential timeline threats through proper project risk assessment.

3. Financial Risks

Financial risks, or cost risks, might include the rising costs of materials, unrealistic budgets, higher-than-expected time or labor requirements, lower-than-expected sales numbers, or the failure to secure sufficient funding.

Here is an example of a financial risk in a marketing project: The team budgets $50,000 for a digital ad campaign based on estimated ad rates. Midway through the campaign, competition drives ad prices much higher than expected, quickly exhausting the budget. The team must either reduce campaign reach or request additional funding, lowering ROI.

Cash flow timing issues, currency fluctuations, and vendor pricing volatility can all pose financial risk. The more teams account for risk during project planning, the better able they will be to adapt and avoid overruns, so make sure to create a solid project risk management plan.

“More accurate budget projections improve the quality of your data. Improved data quality is one of the most critical components of various risk management practices.”

Scope risk, or scope creep, is common in projects of all sizes and types. It happens when expectations for a project’s requirements change after the project begins, which can lead to delays, budget overruns, and reduced overall quality.

Common Causes of Scope Creep:

Unclear priorities and deliverables

New feature requests being introduced without formal approval

Budget and timeline expanding without corresponding adjustments to scope

Imagine a retail company that is launching a project to update its app’s checkout page. The initial project plan outlines a single deliverable, which is to add a “save card for future purchases” feature. Two weeks in, the CEO asks the team to also build a “buy online, pick up in store” option. The project manager agrees, even though it was not in the original plan. A week later, another executive requests a new app color scheme to be included as well. As unplanned requests accumulate, the project’s scope expands, increasing workload, delaying delivery, and raising costs.

“Some projects have emerging requirements, meaning there is no way to get all the requirements at the beginning of the project because people are still figuring out what they want."

Projects with clear guidelines and requirements will run into fewer performance risks than those without.

How to Prevent Scope Creep:

Implement a formal change control process

Create a detailed project charter and scope statement

Set clear expectations with stakeholders about scope boundaries

Use automated workflows and approval processes to control changes

5. Resource Risks

Resource risk is the possibility that the personnel, equipment, or materials required for a project will be unavailable, insufficient, or underperforming when needed. Because every project operates within finite resource constraints, careful planning is essential to ensure teams have the necessary capacity and resources.

Common Causes of Resource Constraints:

Poor resource allocation across multiple projects

Unexpected resource unavailability

Underestimation of resource needs

Over-commitment of shared resources

Difficulty recruiting or retaining qualified staff

Workforce burnout and attrition

Imagine a growing coffee chain that is opening a new store in a popular location. They set a date to open, start working on the build-out inside the storefront, and begin hiring staff for the new location. However, they are unable to find and train quality employees by their targeted open date, so they decide to take employees from existing stores to staff the new one. Each store that has had employees removed is now under more strain. After six months, employees are quitting in droves to find work that is less stressful, leaving the company with even fewer resources.

How to Prevent Resource Constraints:

Conduct resource capacity planning early in the project lifecycle

Align staffing plans with project priorities and timelines

Cross-train team members to reduce single points of failure

Monitor resource utilization and availability regularly

Secure critical equipment and materials in advance

Maintain contingency plans for key resource gaps

Invest in employee satisfaction and appropriate compensation

A Note on Avoiding Human Resource Constraints — Employee satisfaction is essential to maintaining a skilled workforce, and a dissatisfied workforce costs a company money. According to a study by the ADP Research Institute, job satisfaction is higher for well-compensated employees. It is in a company’s best interests to invest in a satisfied workforce.

6. Operational Risks

Operational risk is the risk of weaknesses in project management processes, governance, or execution negatively affecting a project. These risks arise when organizations lack effective oversight, procedures, or operational controls.

For example, if a national retailer rolls out a new POS system across hundreds of stores but lacks a disciplined change control process, configuration changes may be made inconsistently across locations. Without a central system for approving and recording configuration updates, teams apply fixes locally without visibility into changes made at other locations. Store teams implement inconsistent configurations, leading to transaction errors and widespread rework.

Operational risks can also emerge from breakdowns in workforce management, day-to-day process execution, system reliability, vendor performance, or compliance oversight. Because projects rely heavily on coordinated and repeatable operations, even small control failures or execution gaps can compound into significant delays, quality issues, or cost increases.

Common Causes of Operational Risk

Weak or inconsistently enforced project governance

Lack of standardized processes and operating procedures

Inadequate change control or configuration management

Unreliable operational systems or infrastructure

How to Mitigate Operational Risk

Establish and enforce standardized project management processes

Implement disciplined governance and change control practices

Document and regularly review operating procedures

Automate repeatable workflows where appropriate

7. External Risks

External risk is the possibility that factors outside the organization’s control — such as market shifts, regulatory changes, supplier issues, or environmental events — will negatively impact a project.

Here are some common types of external risks:

Regulatory and Legal Risks: Changes in laws or regulations might introduce new obligations to a project, or delay approvals or permits.

Economic Risks: Shifts in market demand, inflation, interest rates, or broader economic conditions might reduce expected returns or increase costs.

Supplier and Vendor Risks: Failures or delays from third-party vendors or service providers can disrupt schedules, increase costs, or degrade project quality.

Environmental Risks: Weather events, natural disasters, pandemics, environmental disruptions, or other events might halt operations or damage assets.

Political Risks: Government instability, trade restrictions, sanctions, or geopolitical conflict can limit market access, disrupt supply chains, or increase regulatory uncertainty.

Competitive Risks: Actions by competitors might erode market share, force price reductions, or accelerate timelines unexpectedly.

External hazards are impossible to predict, but you can take steps to mitigate their impact. For example, a company that has an important production warehouse in Florida can prepare for hurricane season with an employee evacuation plan, a business continuity plan, and a plan to move some critical equipment further inland. They can also implement a policy of actively monitoring weather events and invest in insurance to cover any gaps.

How to Prepare for External Risks:

Maintain contingency funds and appropriate reserves

Secure insurance

Monitor industry news

Develop and test business continuity plans

8. Organizational Risk

Organizational risk is the likelihood of internal business conditions, culture, structure, or shifting priorities negatively affecting a project. These risks arise when leadership alignment, funding stability, or organizational readiness changes during execution.

For example, imagine that an enterprise begins a large ERP implementation, but six months into the project, a new CIO shifts corporate priorities toward cloud migration. Executive support and funding for the ERP initiative weaken, putting the project at risk. In this scenario, the team will have to quickly reassess the project’s strategic fit. If support cannot be restored, the initiative may need to be re-scoped or formally paused.

Common Causes of Organizational Risk:

Shifting executive priorities or strategy changes

Weak or inconsistent executive sponsorship

Organizational restructuring or leadership turnover

Conflicting priorities across departments

How to Mitigate Organizational Risk:

Secure strong executive sponsorship early

Regularly validate that project objectives support business strategy

Monitor organizational changes that may affect project priorities

Implement structured change management and communication plans

Stakeholder risk is the possibility that key stakeholders become misaligned, disengaged, resistant, or have conflicting expectations about project outcomes. When stakeholders do not share a common understanding of goals, timelines, or responsibilities, projects can experience confusion, rework, delayed decisions, and loss of support.

Common Causes of Stakeholder Risk:

Unclear roles and responsibilities

Siloed teams using different tools

Infrequent status updates

How to Mitigate Stakeholder Risk:

Establish clear communication channels and regular updates to keep team members aligned

Clarify roles and deliverables to prevent duplicate work

Provide consistent status reporting and checkpoints for stakeholders

Here is a real-world example of stakeholder risk

A marketing team and product development team are launching a new feature. The marketing team understands the launch date is firm and begins their campaign.

Meanwhile, the development team encounters technical issues and assumes they can delay the launch. Neither team communicates their plans or concerns to the other.

Marketing launches their campaign for a feature that is not ready, damaging customer trust and wasting marketing budget.

How to Prevent Stakeholder Risk:

Define and document stakeholder expectations early

Establish and maintain a regular stakeholder communication cadence

Create a single source of truth for project status and decisions

Use collaboration tools that keep discussions tied to project work

10. Strategic Risks

Strategic risk is the possibility that a project will fail to deliver expected business value due to changing market conditions, flawed assumptions, or shifting priorities.

For example, think of an energy company that invests in building new natural gas infrastructure based on projected long-term demand. During the multi-year project, policy incentives rapidly accelerate renewable adoption, reducing the expected ROI. Even if the project is delivered on time and within budget, the business case may no longer hold.

Strategic risks often emerge when market conditions evolve faster than project timelines or when initial business assumptions prove inaccurate. Because these risks affect the fundamental value of the initiative, they can result in significant opportunity costs and stranded investments.

Common Causes of Strategic Risk:

Flawed or outdated market and demand assumptions

Rapid shifts in customer preferences or technology trends

Competitive disruption

Changes in corporate strategy or investment priorities

Long project timelines that outlast original business assumptions

How to Mitigate Strategic Risk:

Validate the business case with current market data before major investments

Reassess strategic alignment at key project milestones, especially for projects with long timelines

Use phased funding or stage-gate reviews for high-uncertainty initiatives

Internal vs. External Project Risks

Internal and external project risks differ in where they originate and how much control the team has over them. Internal risks, such as scope creep or resource shortages, arise within a company and can often be prevented. External risks stem from outside forces, like market shifts or natural disasters, and can often only be mitigated, not prevented.

Internal risks are typically easier to predict and control through proper planning, training, and resource allocation. Because external risks are typically beyond an organization’s direct control, mitigating external risks involves monitoring external signals and preparing contingency plans.

Residual Risks vs. Secondary Risks

Residual risks are the risks that remain after risk mitigation controls have been implemented, while secondary risks are new risks that arise as a direct result of those response actions. In risk management, residual risk reflects the level of exposure an organization must accept, whereas secondary risk represents the unintended consequences mitigation efforts.

For example, installing a security system may reduce theft risk, keeping the residual risk low. However, this mitigation effort might introduce privacy concerns, which would be a secondary risk.

How to Identify Project Risks

To identify project risks, hold a risk identification workshop to brainstorm potential issues, then document findings in a risk register with owners, impacts, and triggers. Next, plot risks in a probability-impact matrix and conduct a SWOT analysis. Finally, review lessons learned from past projects to catch recurring patterns.

1. Hold a Risk Identification Workshop

Effective risk management begins with identification. Using proven techniques like risk identification workshops helps project teams spot potential issues early, giving them more time to plan a response and reduce negative impacts. These collaborative sessions leverage diverse perspectives and experiences to uncover risks that individuals might miss.

Here are some tips for conducting an effective risk identification workshop:

Schedule workshops during the project initiation phase

Include team members from all functional areas

Consider using prompting frameworks to guide discussion

2. Create a Risk Register

Document all the risks you’ve identified in a project risk register. This serves as the central repository for all identified project risks and is a living document. Keeping an up-to-date risk register helps ensure that nothing falls through the cracks.

Here are the key elements to track in your risk register:

Risk description and potential impact

Probability and severity ratings

Risk owner responsible for monitoring and response

Visually plot risks by likelihood and potential impact using a risk assessment matrix. This tool helps teams quickly identify which risks need immediate attention versus those requiring only periodic monitoring.

These free risk assessment forms use proven techniques like color-coding and simple grid layouts to make risk assessment easy and effective.

4. Conduct a SWOT Analysis

A SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis at the project level allows teams to systematically evaluate internal and external factors that could impact success. Strengths refer to internal capabilities that support project success. Weaknesses are internal limitations that could become risks. Opportunities are external factors that could benefit the project. Threats are external factors that could pose risks to the project goals.

Past projects provide valuable insights into risks your project might face. Mining historical data helps teams predict and prevent recurring issues.

Here are some ways to use past projects to help teams identify potential risks:

Review post-project reports and retrospectives

Identify patterns in past project risks

Build an organizational risk knowledge base

Incorporate industry benchmarks and case studies

Smartsheet provides built-in risk register templates, visual dashboards for risk matrices, and centralized repository for lessons learned across your project portfolio. This makes risk identification systematic and repeatable.

Smartsheet Can Help You Manage and Prepare for Project Risks

Empower your people to go above and beyond with a flexible platform designed to match the needs of your team — and adapt as those needs change.

The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

When teams have clarity into the work getting done, there’s no telling how much more they can accomplish in the same amount of time. Try Smartsheet for free, today.

Frequently Asked Questions About Project Risk Types

The most common types of project risks include schedule, financial, scope, resource, technical, stakeholder, and external risks. They represent the main sources of uncertainty affecting project success. They might mean timeline slippage, overspending, scope creep, staffing gaps, tech issues, stakeholder conflict, and more.

The difference between project-level and business-level risks is scope. Project-level risks threaten project success. They involve specific project execution, like missed deadlines, budget issues, or scope changes. Business-level risks threaten enterprise performance. They include competitive pressures, regulatory exposure, or revenue volatility, which affect the whole organization.

To identify project risks before they occur, perform a structured risk assessment during project planning. Brainstorm with stakeholders, review lessons learned from past projects, and conduct a SWOT analysis. Record potential risks in a risk register and review it regularly to detect emerging threats early.

Project management software helps with risk management by identifying, tracking, and mitigating risks in a single system. It allows teams to log risks in a risk register, assign owners, set alerts, assess likelihood and impact, and monitor changes in real time. This ensures proactive risk response and better decision-making.