Overview of Cost Estimating

Cost estimating is the practice of forecasting the cost of completing a project with a defined scope. It is the primary element of project cost management, a knowledge area that involves planning, monitoring, and controlling a project’s monetary costs. (Project cost management has been practiced since the 1950s.) The approximate total project cost, called the cost estimate, is used to authorize a project’s budget and manage its costs.

Professional estimators use defined techniques to create cost estimates that are used to assess the financial feasibility of projects, to budget for project costs, and to monitor project spending. An accurate cost estimate is critical for deciding whether to take on a project, for determining a project’s eventual scope, and for ensuring that projects remain financially feasible and avoid cost overruns.

Cost estimates are typically revised and updated as the project’s scope becomes more precise and as project risks are realized — as the Project Management Body of Knowledge (PMBOK) notes, cost estimating is an iterative process. A cost estimate may also be used to prepare a project cost baseline, which is the milestone-based point of comparison for assessing a project’s actual cost performance.

Key Components of a Cost Estimate

A cost estimate is a summation of all the costs involved in successfully finishing a project, from inception to completion (project duration). These project costs can be categorized in a number of ways and levels of detail, but the simplest classification divides costs into two main categories: direct costs and indirect costs.

- Direct costs are broadly classified as those directly associated with a single area (such as a department or a project). In project management, direct costs are expenses billed exclusively to a specific project. They can include project team wages, the costs of resources to produce physical products, fuel for equipment, and money spent to address any project-specific risks.

- Indirect costs, on the other hand, cannot be associated with a specific cost center and are instead incurred by a number of projects simultaneously, sometimes in varying amounts. In project management, quality control, security costs, and utilities are usually classified as indirect costs since they are shared across a number of projects and are not directly billable to any one project.

A cost estimate is more than a simple list of costs, however: it also outlines the assumptions underlying each cost. These assumptions (along with estimates of cost accuracy) are compiled into a report called the basis of estimate, which also details cost exclusions and inclusions. The basis of estimate report allows project stakeholders to interpret project costs and to understand how and where actual costs might differ from approximated costs.

Beyond the broad classifications of direct and indirect costs, project expenses fall into more specific categories. Common types of expenses include:

- Labor: The cost of human effort expended towards project objectives.

- Materials: The cost of resources needed to create products.

- Equipment: The cost of buying and maintaining equipment used in project work.

- Services: The cost of external work that a company seeks for any given project (vendors, contractors, etc.).

- Software: Non-physical computer resources.

- Hardware: Physical computer resources.

- Facilities: The cost of renting or using specialized equipment, services, or locations.

- Contingency costs: Costs added to the project budget to address specific risks.

Create Project Cost Estimates at Critical Points in the Timeline

Cost estimates are critical to successful project management, so teams are expected to produce a reasonably accurate and reliable estimate during the conception and definition phase of a project. Estimates are adjusted for accuracy during the planning phase, as project stakeholders and sponsors may ask for revisions before they are willing to authorize a budget. After this early stage, the accuracy of estimates is systematically increased.

Cost estimating is an ongoing process, and estimate revisions are normal in order to ensure accuracy throughout project execution. Typically, work scheduled in the near future will have the most accurate estimates, while work scheduled farther away in time have less accurate estimates. This approach is known as rolling wave planning.

Detailed cost estimates are usually broken down into greater levels of detail and supplementary information. These outputs typically include:

- Activity cost estimates for the activities that make up a project.

- Supporting details, which include assumptions underlying estimates, cost data sources, and cost element sensitivity.

- Requested changes, which a newer, more accurate cost estimate may prompt.

- Updates to the cost management plan, such as those necessitated by changes to the project scope.

- Inputs for subsequent planning processes that use cost estimates.

The Continuum of Accuracy in Project Cost Estimations

Project cost estimates are classified into categories based on how well the scope is defined at the time of estimation, on the types of estimation techniques used, and on the general accuracy of estimates. These categories are not standardized, but they are all based on the recognition that a cost estimate can only be as accurate as the project scope is detailed. In its estimating manual, the American Society of Professional Estimators (ASPE) classifies cost estimates in order of increasing accuracy on a five-level scale. Level 1 is an order of magnitude estimate and Level 5 is a final bid. The U.S. Department of Energy uses a similar five-class scale, but in the reverse accuracy order (Class 5 as an order of magnitude estimate and Class 1 as a definitive estimate).

AACE International (formerly the Association for the Advancement of Cost Engineering) offers a helpful chart summarizing key points. Here’s an overview of the cost estimate categories:

Order of magnitude estimates: An order of magnitude estimate, or ASPE Class 5, is an extremely rough cost estimate created before a project has been defined. It is based only on expert judgment and the costs of similar past projects. An order of magnitude estimate is typically presented as a range of costs spanning -25% to +75% of the actual project cost. It is only used in high-level decision making to screen projects and determine which ones are financially feasible.

Intermediate estimates: An intermediate estimate can be created using stochastic or parametric techniques when a project is defined to some limited extent. Like an order of magnitude estimate, its main purpose is determining project feasibility based on the general project concept.

Preliminary estimates: Created when a project’s deliverables are about halfway defined, a preliminary estimate uses somewhat detailed scope information to incorporate unit costs. Preliminary estimates are accurate enough to be used as a basis for project financing. Some project budgets are authorized based on the preliminary estimate.

Substantive estimates: A substantive estimate uses a reasonably finalized project design to create a fairly accurate cost estimate based mainly on unit costs. At this point, the project’s objectives and deliverables are established, so a substantive estimate is accurate enough to create a bid or tender to complete a project. Substantive estimates may also be used to control project expenditure.

Definitive estimates: Drafted when a project’s scope and constituent tasks are almost fully defined, a definitive estimate makes full use of deterministic estimating techniques, such as bottom-up estimating. Definitive estimates are the most accurate and reliable and are used to create bids, tenders, and cost baselines.

Of course, even definitive estimates do not remain static through project execution. Since all estimates are based on numerous assumptions and are contingent upon risks of all magnitudes, cost estimates are often updated if these base assumptions change significantly or additional risks are realized. When this happens, the project cost baseline is revised accordingly so that you can continue to assess project performance accurately.

Estimates of all types are created using a combination of estimation techniques (with varying levels of accuracy). As we have seen, the most accurate estimates rely more on deterministic methods than on conceptual methods.

Major Cost Estimating Techniques: Best Uses for Each

To create accurate estimates, cost estimators use a combination of estimating techniques that allow for varying levels of accuracy. While the cost estimator always aims to create the most accurate estimate possible, they may have to start with less accurate estimates and revise once project scope and deliverables are fleshed out. The most widely used cost estimating techniques are:

Analogous estimating: Like expert judgment, analogous estimating — also called top-down estimating or historical costing — relies on historical project data to form estimates for new projects. Analogous estimating draws from a purpose-built archive of historical project data, often specific to an organization. If an organization repeatedly performs similar projects, it becomes easier to draw parallels between project deliverables and their associated costs, and to adjust these according to the scale and complexity of a project.

Analogous estimating can be quite accurate if used to form estimates for similar projects and if experts can precisely assess the factors affecting costs. For example, a similar project conducted three years ago might be used as the basis for a new project cost estimate. Adjust the estimate upward for inflation, downward for the amount of resources required, and upward again for the project’s level of difficulty. These adjustments are typically stated as percentage changes — a new project might require 10 percent more preparation time and 15 percent more on resources. However, project management professional Rupen Sharma stresses the need to make sure that projects really are comparable since projects that appear similar, such as road construction, can actually cost vastly different amounts depending on other factors — say, local landscapes and climates.

Bottom-up estimating: Also called analytical estimating, this is the most accurate estimating technique - if a complete work breakdown structure is available. A work breakdown structure divides project deliverables into a series of work packages (each work package comprised of a series of tasks). The project team estimates the cost of completing each task, and eventually creates a cost estimate for the entire project by totaling the costs of all its constituent tasks and work packages — hence the name bottom-up. Bottom-up estimates can draw from the knowledge of experienced project teams, who are better equipped to provide task cost estimates.

While deterministic estimating techniques such as bottom-up estimating are undoubtedly the most accurate, they can also be time-consuming, especially in large and complex projects with numerous work breakdown structure components. It is not unusual for definitive estimates to also use techniques such as stochastic, parametric, and expert-judgment-based estimating (if these have proved suitably accurate in early estimates). That said, bottom-up estimating is also the most versatile estimating technique and you can use it for many types of projects.

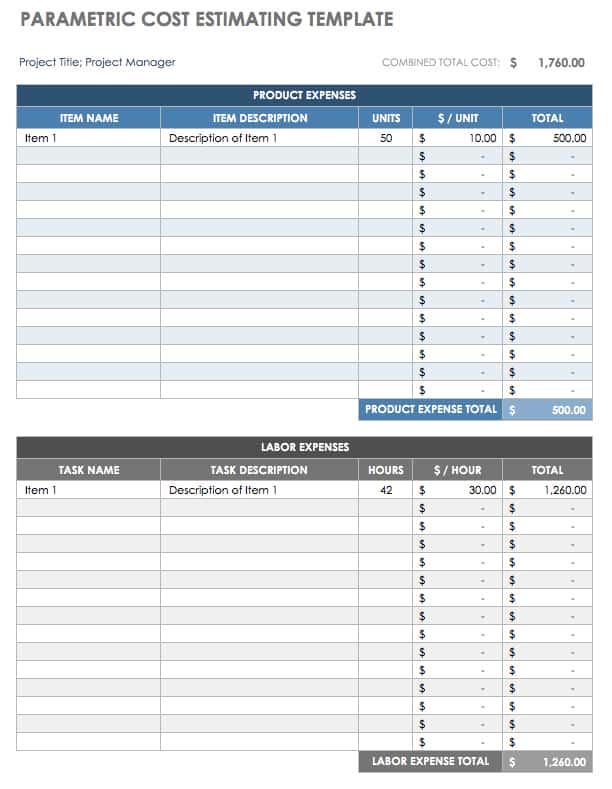

Parametric estimating: For projects that involve similar tasks with high degrees of repeatability, use a parametric estimating technique to create highly accurate estimates using unit costs. To use parametric estimating, first divide a project into units of work. Then, you must determine the cost per unit, and then multiply the number of units by the cost per unit to estimate the total cost. These units might be the length in feet of pipeline to be laid, or the area in square yards of ceiling to be painted. As long as the cost per unit is accurate, estimators determine quite precise and accurate estimates.

However, as project management professional Dick Billows, Chief Executive Officer of 4PM.com, cautions, parametric estimating does not work well with creative projects or those with little repeatability. It is difficult, for example, to come up with an accurate cost per chapter for editing a book written by 12 different authors, since each chapter is likely to require a different amount of work. Similarly, a writer penning a fantasy novel on commission may find herself struggling to advance the story at some points and fully immersed in its flow at others. Therefore, parametric estimating is a good choice only for skill-based projects with uniform, repeatable tasks.

Download Parametric Cost Estimating Template Below

Excel | Word | Smartsheet

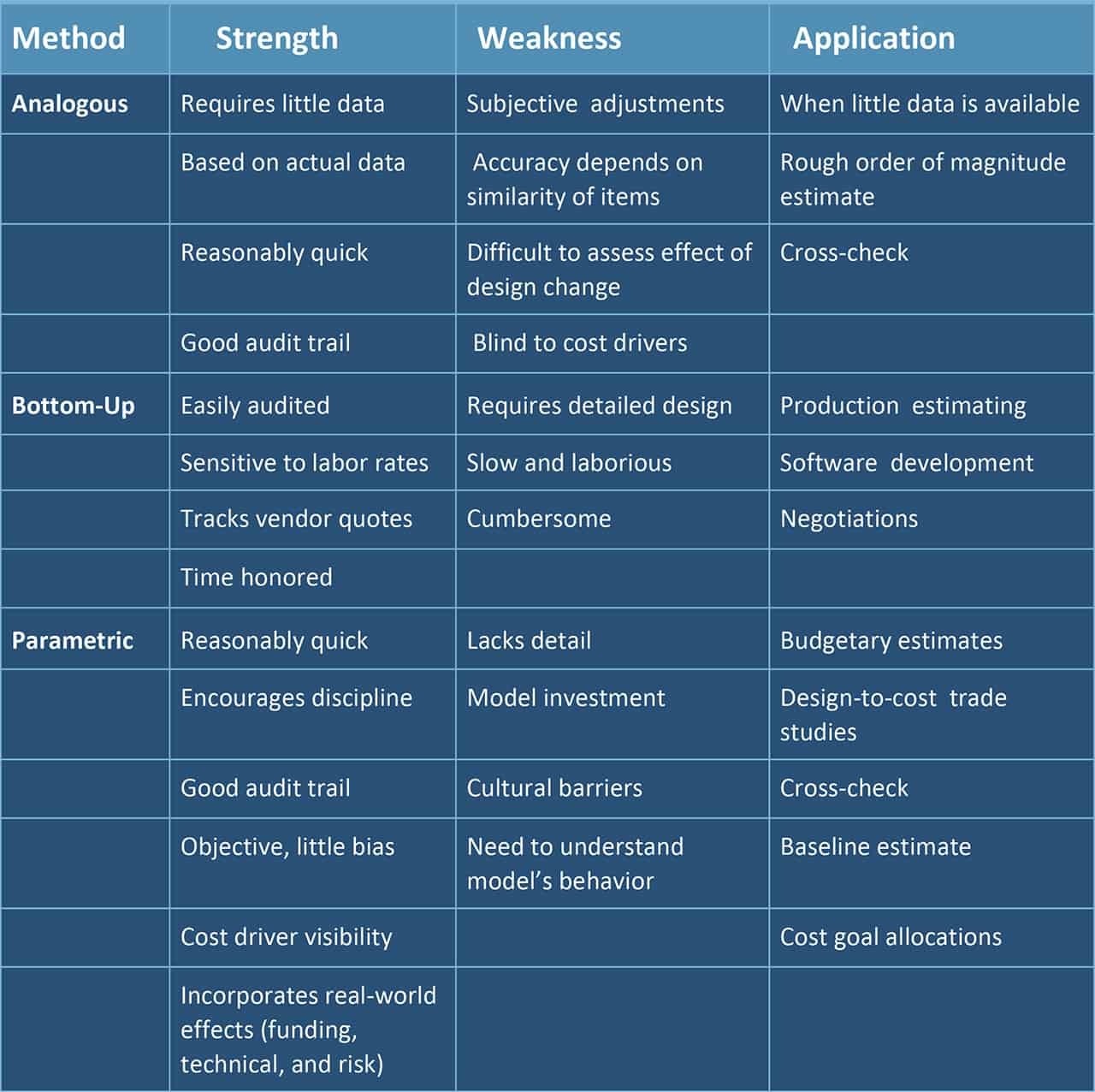

Compare the Strengths and Weaknesses of Analogous, Bottom-Up and Parametric Cost Estimating

Cost of quality: The cost of quality is a concept used in project management - and more broadly in product manufacturing - to measure the financial cost of ensuring that products meet agreed-upon specifications. It usually includes the costs of preventing, identifying, and addressing defects. As an aspect of quality management, the cost of quality is usually an indirect project cost.

Delphi cost estimation: An empirical estimation technique based on expert consensus, Delphi estimation can help resolve discrepancies among expert estimates. A coordinator has experts prepare anonymous cost estimates with rationales; once these anonymous estimates are submitted, the coordinator prepares and distributes a summary of the responses and experts create a new set of anonymous estimates. This exercise is repeated for several rounds. The coordinator may or may not allow the experts to discuss estimates after each round. As the exercise progresses, the estimates should converge (indicating growing consensus between the estimators). When an estimate consensus has been reached, the coordinator ends the exercise and prepares a final consensus-based estimate.

Empirical costing methods: Empirical costing methods draw from previous project experiences using software- or paper-based systems. These methods work well for projects that are similar and frequently conducted in certain industries. A project manager wanting to obtain an empirical cost estimate completes a form detailing the project’s characteristics and parameters, and the system estimates a cost based on the kind of project. Since empirical costing methods draw from existing data and are increasingly automated, they are accurate, time-effective choices for less complicated projects. The Royal Institution of Chartered Surveyors’ Building Cost Information Service (BCIS), which computes rebuilding costs for houses, is an example of an empirical costing method.

Expert judgment: Most commonly used in order of magnitude and intermediate estimates, expert judgment estimating is conducted by specialists who know how much similar projects have cost in the past. As such, it relies mainly on drawing parallels between past and future projects to create and adjust estimates. Since any two projects are unlikely to be identical and project work is typically complex, expert judgment estimates are presented as a range. While a wide range typically means these estimates have limited use, project management professional Billows points out that such broad estimates are only meant to indicate project feasibility and provide a ballpark figure to hold project managers accountable. In this regard, they “are better than commitments you can’t keep,” Billows says.

Reserve analysis: Reserve analysis is an umbrella term for a number of methods used to determine the size of contingency reserves, which are budgetary allocations for the incidence of known risks. One outcome of reserve analysis is a technique called padding, which involves increasing the budgeted cost for each scheduled activity beyond the actual expected cost by a fixed percentage. Critical path activities may have larger percentages assigned as padding. The Project Management Institute (PMI) also suggests other methods for managing contingency reserves, including the use of zero-duration activities that run in tandem with scheduled activities and the use of buffer activities that contain both time and cost contingency reserves.

Resource costing: Resource costing is a simple mathematical method to compute the costs of hiring resources for a project. It is easily done by multiplying the hourly cost of hiring a resource by the number of projected employment hours.

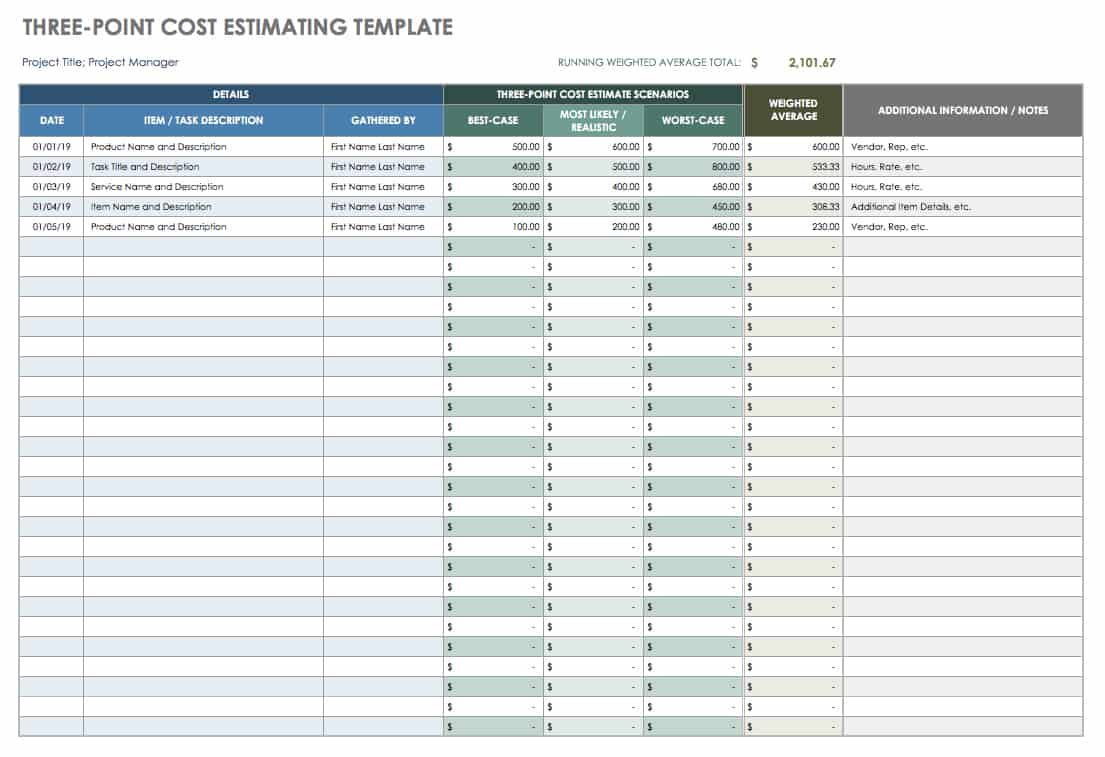

Three-point estimating: Three-point estimating has roots in a statistical method called the Program Analysis and Review Technique (PERT), which is used to analyze activity, project costs, or durations by determining optimistic, pessimistic, and most likely estimates for each activity. Three-point estimating uses a variety of weighted formula methods to compute expected costs/durations from optimistic, pessimistic, and most likely costs/durations. One commonly used formula for creating estimates is:

Expected value = [Optimistic estimate + Pessimistic estimate + (4 x Most likely estimate)] ÷ 6

The standard deviation is also calculated to create confidence intervals for estimates:

Standard deviation = (Pessimistic estimate – Optimistic estimate) ÷ 6

Three-point estimating can construct probability distributions of estimates in a number of fields. In project cost estimating, estimators may create a three-point estimate of cost using optimistic, pessimistic, and most likely costs. Alternatively, for projects that measure deliverables in units of time with fixed costs, estimators may use expected durations as the number of units and determine costs via parametric estimates. However, remember that three-point estimates are only as good as their initial optimistic, pessimistic, and most likely estimates - if these are not accurate, the expected values are useless.

Download Three-Point Cost Estimating Template - Excel

U.S. Government Accountability Office (GAO) 12-step process: The GAO recommends a 12-step process for creating high-quality cost estimates. Essentially a deterministic estimating technique, the 12-step process is a systematic approach where estimators select an appropriate estimating technique for each component of a work breakdown structure, fully identify the assumptions underlying estimates, and conduct risk and uncertainty analyses for estimates.

Using cost estimating software: Project management software can simplify, speed up, and enhance cost estimating. You can use a variety of project management software to create cost estimates or to determine the levels of uncertainty involved in cost estimates via probabilistic modeling.

The Monte Carlo method is one example of this modeling approach. It refers to the risk analysis simulations performed by researchers working on the atomic bomb and named after the gambling resort in Monaco. The Monte Carlo method produces a range of potential outcomes and offers probabilities for their occurrence based on different variables.

Vendor bid analysis: This estimating technique is used to supplement internally constructed estimates. It allows estimators to compare their own estimates with those stated in bids submitted by vendors, and can provide a useful point of comparison and external perspectives on what a project should cost.

What Makes a Good Cost Estimate?

The usefulness of a cost estimate depends on how well it performs in areas like reliability and precision. There are several characteristics for judging cost estimate quality. These include:

Accuracy: A cost estimate is only as useful as it is accurate. Aside from selecting the most accurate estimating techniques available, accuracy can be improved by revising estimates as the project is detailed and by building allowances into the estimate for resource downtime, project assessment and course correction, and contingencies.

Confidence level: Since even the best estimates contain some degree of uncertainty, it is important to communicate the amount of potential variability in any estimate to stakeholders. Confidence levels can communicate estimates as ranges, such as those produced by three-point estimating techniques or Monte Carlo simulations.

Credibility: Stakeholders or sponsors preparing to authorize budgets want to know that estimates are founded in established fact or in practical experience. Increase the credibility of an estimate by incorporating expert judgment and by using set values for variables, such as unit costs and work rates.

Documentation: Since project managers are eventually held accountable to cost estimates, it is important that the assumptions underlying estimates are identified and recorded in writing, and that regular budget statements are provided. Thorough documentation precludes misunderstandings and helps stakeholders understand the reasons behind estimate revisions.

Precision: To reduce the variation in cost estimates due to techniques used, estimators should compare and corroborate estimates. Cost estimating software makes this fairly easy.

Reliability: Reliability is a concept based on the extent to which historical cost estimates for a certain type of project have been accurate. For new projects that are similar to successfully-completed past projects, analogous estimating techniques will allow reliable estimates.

Risk detailing: All projects can be affected by negative risks, so it is important to build allowances into cost estimates. Thorough risk identification and allocation of contingency reserves is the most common approach. Estimates should be overestimated rather than underestimated, and estimators should establish tolerance levels for cost deviation.

Uniformity: For performing organizations that conduct many projects of the same type, expect unit costs to be reasonably consistent across projects and only adjusted for inflation. This type of unit cost uniformity is possible for organizations that have undertaken several similar projects, which enables them to create reference lists for recommended unit costs.

Validity: Confirming the validity of a cost estimate involves checking the underlying data for accuracy. Improve validity by relying on established cost literature, and on cost indices when up-to-date literature is unavailable.

Verification: Cost verification is the act of checking that mathematical operations used in an estimate were performed correctly. Cost verification is much easier if estimates are properly documented.

In their book Project Management for Business, Engineering, and Technology, project management experts John M. Nicholas of Loyola University and Herman Steyn of University of Pretoria, South Africa, say the best estimates are made by teams that include designers, builders, suppliers (this is opposed to estimates from more homogenous teams). They describe these diverse estimating teams as concurrent engineering teams.

The Most Likely Causes of Inaccurate Project Cost Estimates

Alternatively, factors that undermine cost estimations include poor raw data or assuming that resources are 100 percent utilized. Some of the most common pitfalls for cost estimators are:

Lack of experience with similar projects: Accuracy in cost estimating tends to increase as estimators, project teams, and organizations gain experience working with similar projects. Inexperienced estimators and project teams may not be familiar with the scope of a project, which may lead to inaccuracies with - even with deterministic estimating techniques. At an organizational level, the use of analogous estimating techniques is typically not reliable if the organization has not conducted similar projects before.

Length of the planning horizon and of the project: Professional estimators stress the importance of not making premature estimates. As we have discussed, accurate estimating depends on the degree to which a project is defined. For large, complex projects, approaches such as rolling wave planning mean that future work is less well defined. It is important that cost estimating practices reflect this and that cost estimates are revised as more up-to-date information becomes available. For mega projects that take several years to complete, it’s important to take currency value fluctuation and political climates into account.

Human resources: Creating accurate estimates becomes more difficult as the number of human resources involved in a project increases. While it is standard practice to assume that any resource will only be productive 80% of the time and to create estimates accordingly, it becomes harder to account for costs in managing and organizing people. This is especially noticeable in project activities that involve building consensus or coordinating tasks across many people.

Difficulty also arises when estimating costs of human resources via resource costing or parametric estimating. Both estimating techniques revolve around the concept of unit-based costing, but the complexities of managing people make it difficult both to obtain accurate unit costs and to forecast the task completion time accurately. Further, it’s unlikely that workers’ skill levels will be identical (even if they are classified as such), so some time deviation is inevitable. This shows the value of systematically overestimating instead of underestimating, especially when dealing with human workers.

Several other common mistakes can affect the accuracy of estimates:

Not fully understanding the work involved in completing work packages: This is sometimes a problem for inexperienced project teams who have not worked on similar projects before.

Expecting that resources will work at maximum productivity: A more appropriate rule of thumb is to assume 80% productivity.

Dividing tasks between multiple resources: Having more than one resource working on a task typically necessitates additional planning and management time, but this extra time is sometimes not taken into account.

Failing to identify risks and to prepare adequate contingency plans and reserves: Negative risks can both raise costs and extend durations.

Not updating cost estimates after project scope changes: Updated cost estimates are an integral part of scope change management procedures, as project scope changes render prior estimates useless.

Creating hasty, inaccurate estimates because of stakeholder pressure: Since project managers are held accountable for estimates, order of magnitude estimates are a much better choice than numbers pulled out of thin air.

Stating estimates as fixed sums, rather than ranges: Point estimates are misleading. All estimates have inherent degrees of uncertainty, and it is important to adequately communicate numbers like cash flow via estimate ranges.

Making a project fit a fixed budget amount: The scope of a project should determine its budget, not the other way around. As Trevor L. Young explains in his book How to be a Better Project Manager, estimating is a “decision about how much time and resource are required to carry out a piece of work to acceptable standards of performance.” The reverse approach — planning projects to fit budgets — is likely to result in projects that fail to meet requirements and to deliver results.

Other Project Management Fields Tie to Cost Estimating

The job of estimating project costs and ongoing budget control is not done in a vacuum. Several other project management specialties influence it, and the cost estimation, in turn, has impact on those other project aspects. Some of these are:

Communications management: Routinely update project team members and stakeholders with project activities. Project team members who do not understand their roles cost the project time and money. Likewise, stakeholders who do not receive regular project progress updates may request costly management changes at non-optimal times.

Human resource management: Inadequately trained or unprepared project staff can be a liability in terms of both time and money.

Procurement management: Ineffective procurement management can increase project costs, especially for projects performed over extended lengths of time. For example, fluctuating resource prices and changing economic and political conditions may make it more expensive to procure necessary goods or services.

Quality management: Establish quality requirements for project deliverables before execution begins, and communicate these requirements to all project team members. A lack of clarity on quality requirements can prove costly during the quality control process, when defects or noncompliance must be addressed (often at substantial cost).

Risk management: All projects face risks. Adequate risk identification and preparation of contingency plans and reserves are vital to prevent risks from causing cost overruns.

Time management: Project costs are directly related to the time taken to complete a project, and so a failure to construct an accurate and viable project schedule will likely cause cost overruns.

How Cost Estimation Is Applied in Key Industries

Regardless of the size and scope of your project, standardized cost estimating will help produce accurate estimates. That said, the industry, sector, and type of project can have a bearing on how you develop your estimates. Therefore, it’s worth examining how cost estimating is done in some key industries and more complex use cases.

Construction

Construction costs span two major cost categories: those incurred in the actual construction and development of a facility and those incurred in the operations and maintenance of the facility throughout its life cycle.

The first category includes things like the cost of land, labor, equipment, and materials needed to build a facility, the cost of architectural design and engineering, and the cost of facility inspection. The second category includes maintenance and repair costs, land rent and utilities costs, and the cost of operations and employing operations staff.

One factor that looms large in cost estimation for construction projects is the need for contingencies. Since construction projects are typically large-scale and performed over extended periods of time, adequate contingency planning is vital. Contingencies in construction projects include:

- Schedule adjustments, which are not unusual for such large-scale projects. Given the large costs of equipment and labor in construction projects, delays and schedule extensions can increase costs considerably.

- Changes in equipment and labor costs, which are also not uncommon in lengthy projects.

- Environmental changes, such as changes in climate — again not uncommon in lengthy projects.

- Changes in design development, which, though rare, are not unheard of. These depend on the quality of pre-execution project planning and uncontrollable circumstances such as natural events.

Cost estimates for construction projects fall into three classes:

- Design estimates: Created during project planning and design, these include a number of estimates ranging in accuracy from screening through conceptual to definitive.

- Bid estimates: This is a finalized definitive estimate used to conduct competitive bidding.

- Control estimates: Use these to measure cost performance during project execution; they are susceptible to revisions during a project.

An important aspect of cost estimation in construction projects is determining the relationship between project scale and average cost per unit. Typically, estimators using empirical data to establish these relationships will find that there are economies or diseconomies of scale. That is, the average cost per unit changes as the scale of the project increases. Estimators seek to take advantages of economies of scale to minimize unit costs.

Information Technology

In producing cost estimates for information technology projects, many of the conventional cost estimation practices do not adapt well to Agile project development, given this approach’s emphasis on changing project scopes.

However, since the primary input in Agile processes is labor - not resources - and that Agile development supports fixed-time iterations, use parametric estimating techniques to create accurate cost estimates. Agile development teams divide work into manageable portions for each iteration and can thus charge fixed costs depending on the number of developers needed to complete the work scheduled for each iteration.

Even here, however, there may be difficulties. Fixed price cost estimating works well for adaptation work, which focuses mainly on amending already designed IT products. Developmental work, on the other hand, is more difficult to estimate, given that it involves product design. Because Agile methods encourage scope changes, it is difficult to pre-plan the amount of time to spend on design. Therefore, cost overruns for developmental work are quite common.

On the whole, therefore, cost estimation for IT development projects (involving both developmental and adaptation work) is best conducted as a combination of top-down and bottom-up estimating. Adaptation, which is generally well defined, can be estimated using bottom-up estimating techniques since its scope is fixed. Developmental work, which does not have a fixed scope, is better estimated using top-down techniques such as expert judgment and analogous estimating.

Engineering

Civil engineering projects (such as for highways and bridges) sometimes have added pressure from increased public interest in their progress and especially their cost performance. This can be problematic when critics fail to appreciate the iterative nature of cost estimating and draw misleading comparisons between inaccurate preliminary estimates and control estimates. This problem is compounded by the fact that civil engineering projects typically feature large degrees of uncertainty in estimates — usually due to a combination of project length, natural conditions, and, in some instances, political conditions in the region. As such, organizations such as The Institution of Engineers of Ireland suggest that preliminary estimates for civil engineering projects not be made public and that more definitive estimates clearly state project scopes and underlying assumptions.

Civil engineering projects that run over extended periods of time may also have to contend with scope changes requested by changing political administrations. In some developing countries, these projects might struggle to retain political support as governments change, and it is not uncommon for there to be problems with administrative corruption. As such, civil engineering projects place special importance on adequate risk identification, and contingency reserves for these projects tend to be generous. It is also important to undertake project planning in a way that minimizes the likelihood of future scope changes, since these can easily cause cost overruns.

Service Industries

Project costing in service industries can present a unique set of challenges. Since the emphasis is on knowledge-based work (for which expected durations and rates of work can be difficult to forecast), simple, unit-based estimating techniques are unsuitable. Instead, service industry projects typically compute labor and resource costs separately, and add overhead costs to these when creating estimates.

Costs for service industry projects are broadly divided into three categories: labor costs, resources, and overheads. In most cases, labor and resource costs are simply billed as they are incurred on a per-job basis. Billing for overheads, however, is more complicated, especially since increased automation has in recent years increased the size of overhead costs for many service industries. Service industries adopt a variety of costing techniques to manage billing for overhead costs, including:

- Job order costing: Applies a fixed overhead fee to each job.

- Activity-based costing: Assigns overheads in proportion to service activities via cost drivers.

- Actual costs plus: Assigns a percentage of a company’s actual costs as overheads to each job.

- Set costs: Charges each job a predetermined fixed fee.

Set costs jobs are, of course, the easiest to estimate. For the other costing techniques, the separation of resource costs from labor costs can improve the accuracy of estimates as long as service providers can accurately assess the extent of labor involved in each project — which can be imprecise.

Commonly Used Tools for Cost Estimating

Empower your people to go above and beyond with a flexible platform designed to match the needs of your team — and adapt as those needs change.

The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

When teams have clarity into the work getting done, there’s no telling how much more they can accomplish in the same amount of time. Try Smartsheet for free, today.